Chris Gottschalk

Chris Gottschalk

1 min read

5 Easy Steps To Financial Literacy For Beginners

Did you know that, according to one report, almost half of Americans make a New Year’s Resolution related to finance? If you’re one of those people,...

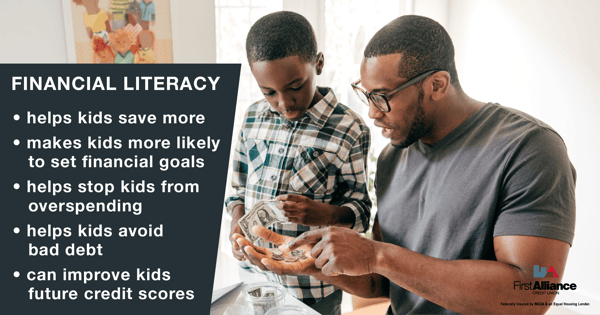

When you teach your kids financial literacy—the knowledge and skills you need to make effective, informed decisions about money management—you're giving them a set of skills that will benefit them for the rest of their lives.

This may sound like an exaggeration, but it's not. According to a 2015 study by the Financial Industry Regulatory Authority, or FINRA, teaching children to be financially literate before they enter college or join the workforce is essential to helping them achieve financial security and success.

One of the core aspects of financial literacy is learning to save. When kids develop good savings habits, they carry those habits with them into adulthood. This can really help set them up for financial success later in life, especially when they understand how compound interest lets their money in their savings account or investment account earn money.

According to a 2014 interview with the academic director at the Global Financial Literacy Excellence Center, if kids knew to start saving for the future at age 20 instead of age 50, it would make a huge difference in their financial security. Having good savings habits can also help them achieve big financial goals when they grow up, such as buying a new car or a new house.

Speaking of which…

Another key aspect of financial literacy is being able to set financial goals. Specifically, children should be taught to set goals that are S.M.A.R.T.—Specific, Measurable, Achievable, Relevant and Time-bound.

When kids learn to set and achieve smaller S.M.A.R.T. financial goals, they’ll be more likely to set and work towards larger financial goals when they grow up. That means they’ll be less prone to spend their money on impulse buys and more likely to save for the things that really matter to them as adults.

When you’re in the habit of saving regularly and working toward a financial goal, you start to appreciate the value of money. You know how much money the things you want cost and you know how much you’ll have to work for them. The natural result is that you become less likely to overspend.

This benefit cannot be overstated. According to a 2013 report, 75% of renters between the age of 18 and 24 spend more than they earn every month, and more than 20% of them overspend their income by $100 every month, putting the amount they overspend on a credit card. That’s an annual debt of $1200 each year.

When kids are financially literate, they understand what going into debt means. As a result, they know to use credit cards and loans to take on good debt to advance their financial goals, putting them in a better situation. Even better, when they do borrow money, they’ll be more likely to get a loan with lower interest rates and pay them off faster, which will save them money in the long run.

All the above benefits of learning to manage money effectively will also impact a young person's credit score once they grow up and start needing to access credit for things like a car loan. This base financial knowledge can help a young person who is going out on their own in many ways. They can get lower interest rates on loans, get higher credit limits and even get approved for loans a peer with a lower credit scores might not.

When children learn financial literacy, it gives them an advantage that will last for the rest of their life. They won’t be intimidated by financial concepts, and they’ll be able to make intelligent financial decisions and avoid the pitfalls that ensnare many people who haven't been taught these important financial skills.

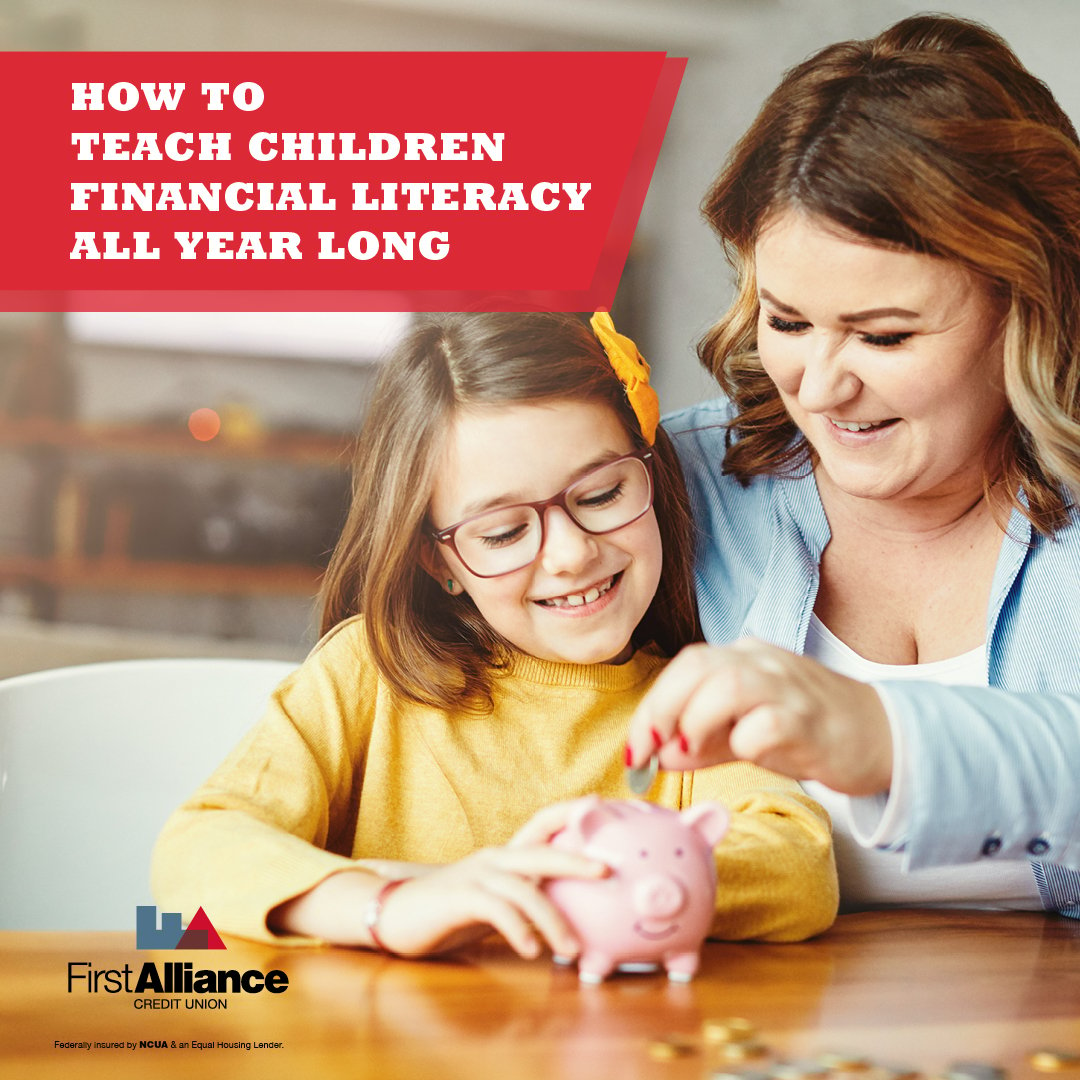

You can help your children learn more about financial literacy when you help them become a member at First Alliance Credit Union today. You can get them a youth account for only five dollars, then help them prepare for financial success by participating in Youth Financial Literacy Month activities.

1 min read

Did you know that, according to one report, almost half of Americans make a New Year’s Resolution related to finance? If you’re one of those people,...

1 min read

April is Youth Financial Literacy month, and as part of this several credit unions, including First Alliance, are putting on programs to help...

1 min read

What is financial literacy and why is it important? Financial literacy is the ability to understand the important financial topics related to...