1 min read

3 Things you Must Know About HELOC Payments

If you’re trying to figure out how to fund your home improvement project, you may have heard about a home equity line of credit, or HELOC. If you...

5 min read

A HELOC (Home Equity Line of Credit) lets homeowners borrow against the equity in their home through a revolving credit line. Unlike a traditional loan, you draw funds as you need them, repay them, and borrow again. Payments are often interest-only during the draw period, then shift to principal and interest during the repayment period.

If you’ve seen the term and wondered what it actually means day to day, you’re not alone. Home equity products come with a learning curve, especially when it comes to understanding how payments change over time. Here’s everything you need to know about how a HELOC works, from the draw period through repayment and beyond.

A home equity line of credit, or HELOC, is a type of loan that lets you borrow against the equity you’ve built in your home. Equity is simply the difference between what your home is worth and what you still owe on your mortgage.

For example, if your home is worth $300,000 and you owe $180,000 on your mortgage, you have $120,000 in equity. A HELOC lets you tap into a portion of that equity and use it kind of like a credit card: you’re approved for a maximum credit limit, and you can borrow from it as needed rather than taking everything in one lump sum.

This flexibility is one of the main reasons homeowners find HELOCs appealing. Whether you’re managing a renovation in stages, handling unexpected expenses, or consolidating higher-interest debt, having access to funds on your own timeline can feel like a real relief.

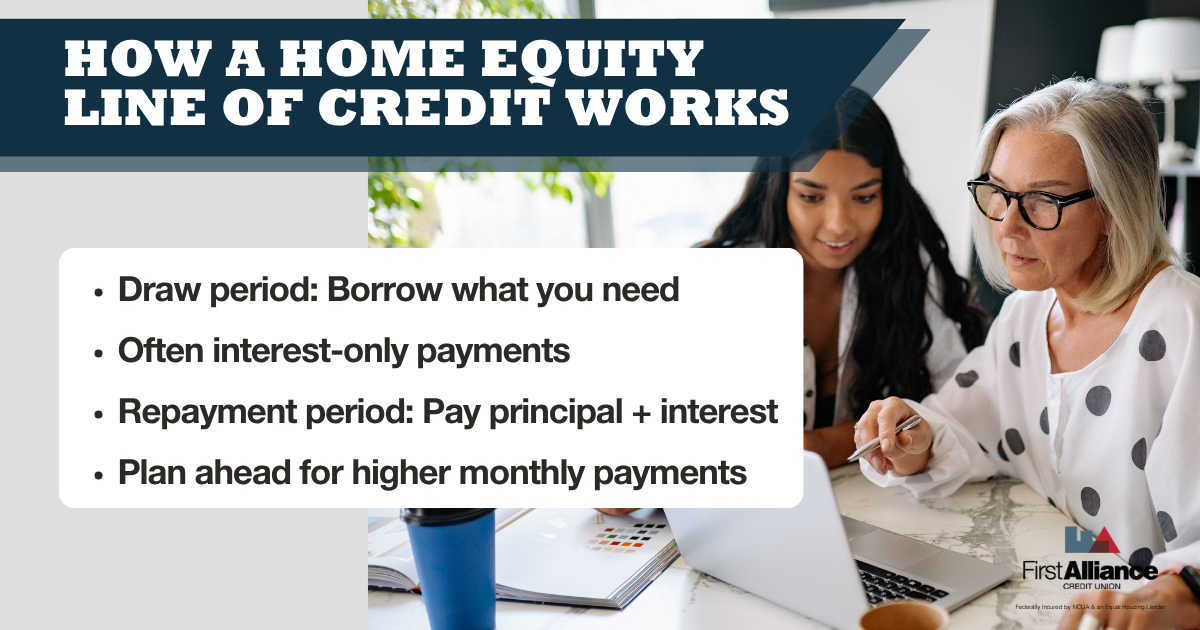

Understanding a HELOC means understanding its two main phases. A lot of the confusion people have around home equity line of credit payments comes from not knowing that these two periods work very differently.

The draw period is the first phase of a HELOC, and it’s when you have access to your credit line and can borrow from it. This phase typically lasts 5 to 10 years, though it can vary depending on your lender and loan terms.

During the HELOC draw period, you can borrow money, pay it back, and borrow again, just like a revolving credit card. One of the most common questions we hear is: Are HELOC payments interest-only at first? In many cases, yes. During the draw period, some HELOCs only require you to make interest payments on what you’ve borrowed. This keeps your monthly payment lower while you’re actively using the funds.

It’s worth noting that even if interest-only payments are all that’s required, you’re always welcome to pay down the principal during this time. Doing so can reduce what you’ll owe later and lower your overall cost of borrowing.

Once the draw period ends, your HELOC enters the repayment period. At this point, you can no longer borrow from the line of credit, and your focus shifts entirely to paying back what you borrowed.

The repayment period typically lasts 10 to 20 years. During this phase, your payments will include both principal and interest, which means your monthly payment will likely be higher than it was during the draw period. This is something to plan for ahead of time so it doesn’t catch you off guard.

Take the guesswork out of HELOC repayment. Talk to the experts at First Alliance Credit Union to walk through the numbers, explore your options, and find a repayment plan that fits your financial goals before you open a line of credit.

Here’s a quick way to picture how a HELOC is structured:

| Draw Period (Typically 5-10 years) | Repayment Period (Typically 10-20 years) |

| Borrow as needed from your credit line | No new borrowing from the credit line |

| Pay interest only on what you see | Pay principal and interest each month |

| Repay and re-borrow as your needs change | Monthly payments are higher than before |

| Flexible access throughout the draw period | Fixed timeline to pay off your balance |

Each phase has its own rules and payment structure. Knowing which one you’re in at any given time helps you plan your budget with confidence and avoid any surprises down the road.

This is one of the most common questions homeowners ask, and for good reason. These two products are related but work quite differently.

| Feature | HELOC | Home Equity Loan |

| How you receive funds | Revolving credit line (borrow as needed) | Lump sum upfront |

| Interest rate | Usually variable | Usually fixed |

| Draw period payments | Often interest-only | Not applicable |

| Best for | Ongoing or unpredictable expenses | One-time, known expenses |

| Flexibility | High | Lower |

A home equity loan gives you a fixed amount upfront with a set repayment schedule, which can be great for a single large purchase like a new roof or a major home addition. A HELOC, on the other hand, gives you flexibility to draw funds over time, which works better for projects or needs that unfold gradually.

Neither option is better across the board. It really comes down to what you’re trying to accomplish.

A HELOC can be a smart borrowing option in a few different situations:

If you’re redoing your kitchen this year and planning to tackle the bathrooms next year, a HELOC lets you borrow what you need when you need it, rather than paying interest on a large lump sum all at once.

Some homeowners use a HELOC to pay off higher-interest debt like credit cards. Since a HELOC is secured by your home, the interest rate is often lower than unsecured debt. That said, this strategy requires discipline, because you’re trading unsecured debt for debt that’s tied to your home.

Having an open line of credit you can draw from in a pinch can provide peace of mind. Just keep in mind that using your home as collateral means it’s important to borrow responsibly.

If you’re not sure exactly how much you’ll need or when you’ll need it, a HELOC’s flexibility can be a better fit than a fixed loan.

A HELOC might not be the right fit if you prefer predictable, fixed monthly payments from the start, or if you’re concerned about variable interest rates potentially rising over time.

Home equity products come with a lot of unknowns, and that's completely normal. Here are the questions members ask us most, along with straightforward answers to help you feel more confident.

A HELOC is a revolving line of credit secured by your home’s equity. You borrow what you need during a draw period, typically pay interest only during that time, and then repay the principal and interest during the repayment period.

The draw period is the phase when you have active access to your credit line and can borrow from it. It usually lasts 5 to 10 years. During this time, minimum payments are often interest-only.

Once the draw period ends, you can no longer borrow and must begin repaying both the principal and interest. This phase typically lasts 10 to 20 years and results in higher monthly payments.

In many cases, yes. Many HELOCs allow interest-only payments during the draw period, which keeps your payment lower while you’re actively using the funds. However, some HELOCs may require principal payments during the draw period depending on your lender’s terms.

A home equity loan provides a lump sum with a fixed interest rate and set repayment schedule. A HELOC gives you a revolving credit line with a variable rate and more flexibility. The right choice depends on your specific needs and financial situation.

If this post got you thinking about whether a HELOC might be a good fit for your situation, the next best step is to have a real conversation with someone who can look at your specific numbers. You’ve worked hard to build equity in your home. Understanding your options is the first step to using it wisely, and we’re here to help you do exactly that.

1 min read

If you’re trying to figure out how to fund your home improvement project, you may have heard about a home equity line of credit, or HELOC. If you...

1 min read

When you buy a house, you’re not just getting a nice place to call your own. You’re also buying one of the few assets that tends to increase in value...

1 min read

In the past, we’ve talked about financial concepts that might be a bit tricky to understand, like a personal loan or an escrow account. With both of...