Chris Gottschalk

Chris Gottschalk

1 min read

5 Things to do With the Child Tax Credit Payments

If you’re a parent, you might have gotten a pleasant surprise from the IRS in the past week. Thanks to the American Rescue Plan which the federal...

With the rise of gig workers in the United States, many people are finding that their employer is giving them a 1099 form instead of a W-2.

At first glance, there isn’t much difference between the two. They have similar fields, and most of them contain the same information. However, there are some big differences between a W-2 form and a 1099 form. Knowing what they are can help you avoid getting in trouble with the IRS.

The main difference between a 1099 form and a W-2 form is that W-2 forms are given to full-time employees, while 1099 forms are records of money you received from a person or entity other than your employer. Since freelancers and gig workers are considered independent contractors rather than full-time employees, they get 1099 forms.

This is a big difference, tax-wise. If you’re a full-time employee, your employer will automatically deduct payroll taxes from your paycheck and pay them to the government on your behalf. If you’re an independent contractor, though, you’re responsible for paying your own taxes to the government.

Independent contractors aren’t the only people who get 1099 forms, though. You might have read the description of a 1099 form in the previous section and realized that “records of money you receive from a person or entity other than your employer” can cover a LOT of situations, from earning interest in a savings account to getting birthday money from your grandma.

Fortunately, the IRS isn’t going to kick down your door because you got $20 from your Mee-maw. However, they do provide 15 different types of 1099 forms for different types of ways you might receive money. Here’s a quick look at them:

If your mortgage lender canceled some or all of your mortgage, the amount of money you saved counts as taxable income in the eyes of the IRS.

This form covers sales of securities, such as stocks, options or commodities. It’s also required if you barter with another business to trade one service for another, like a dentist offering to clean a contractor’s teeth in return for them remodeling her home kitchen.

If you settled your debt with a lender for less than you owe, this counts as taxable income.

If you held shares in a corporation and received cash, stock or other property as the result of that corporation getting acquired or going through a similar big change in their structure, you’ll need to report that as income to the IRS.

This type of 1099 form covers money you make from the dividends you receive from an investment. This doesn’t cover the dividends you get from your First Alliance Credit Union share account, though. That’s classified as interest, and you might see it on the 1099-INT form.

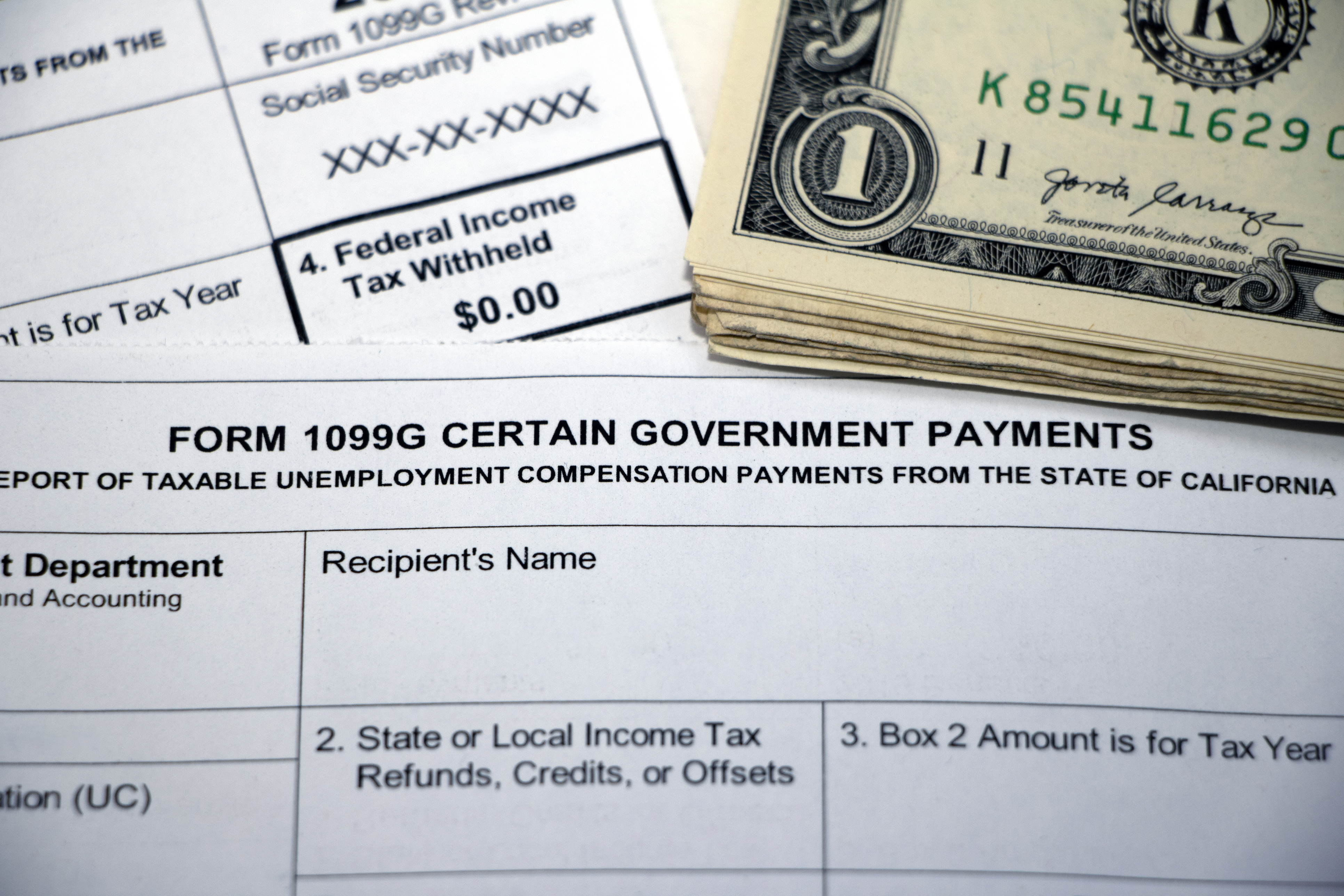

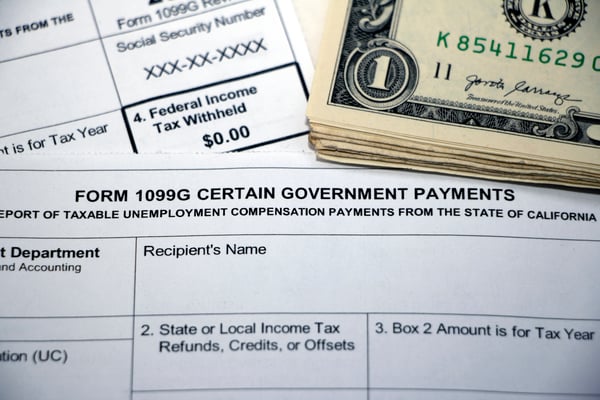

Did you get money from the state, local or federal government this year, like a tax refund or credit? If so, you’ll probably get a 1099-G form. You should know, however, that the stimulus money everyone received earlier in the year doesn’t count as taxable income, so you won’t owe taxes on it.

Here’s where you may have to report the interest your credit union share account earned. If you made over $10 in interest from a financial institution, you’ll have to report that money to the government.

If you received any benefits from long-term care insurance or got payments from the accelerated death benefits of a life insurance policy, you’ll get this form.

This is the form you get when you receive money for any reason not covered by the other types of 1099 forms. The most common places you’ll see this is if you win a cash prize or get a substantial award. Independent contractors used to get this type of form, but the IRS created a new form for them.

The new form the IRS created for independent contractors.

If you bought a financial instrument like a bond at a discount to its face value, you’ll get one of these forms.

If you got at least $10 in patronage dividends to a co-op, you’ll can expect to see this type of 1099 form show up.

This is an unusual type of 1099 form. It reports the money received from a 529 plan. However, since the money a 529 plan earns is generally not considered taxable income so long as it’s used for qualified education expenses, this form is usually just for record-keeping purposes.

This form covers any taxable money you receive from a pension, retirement plan, IRA, annuity or profit-sharing program. It may also cover any loans you took from your retirement plan. Oddly enough, you might also get this type of 1099 form if you received any permanent or total disability payments under a life insurance contract.

If you closed a sale or exchanged real estate, you’ll get this type of 1099 form that reports the proceeds. Keep in mind, though, the proceeds on this type of sale aren’t necessarily taxable, so you may want to consult a financial advisor or CPA.

If you got any distributions from a health savings account, you’ll receive this type of 1099. However, similar to a 529 plan, distributions from a health savings account aren’t taxable as long as you use them for a qualified health expense, so a 1099-SA form is usually used for record-keeping purposes.

Understanding 1099 forms can be a huge help around tax time. It not only helps you figure out what income is taxable, but it also helps you keep track of what types of taxable income you earned.

You can get some more help for tax time when you become a member of First Alliance Credit Union. We offer discounts on TurboTax in our resource center, as well as the opportunity to have a free counseling session with our partners at Green Path Financial Wellness. You can also take advantage of our traditional savings accounts and club savings accounts to save a percentage of your independent contractor salary for tax time. You can even get your tax return put into your checking or savings account by direct deposit.

1 min read

If you’re a parent, you might have gotten a pleasant surprise from the IRS in the past week. Thanks to the American Rescue Plan which the federal...

1 min read

When you get your tax refund, the more you know about how to use it wisely, the better. (We've actually written a couple of blog posts on the subject...

1 min read

While no one likes filing their taxes, most Americans look forward to getting a tax refund deposited into their account. Once you’ve filed your tax...