1 min read

What the Heck is a Personal Loan?

If you go to a credit union or bank's website and search for information about loans, you'll immediately notice that most types of loans are...

5 min read

If you’ve been living with a leaky faucet, outdated flooring, or a bathroom that’s seen better days, you already know that home repairs have a way of moving from “someday” to “right now” faster than you’d like. The harder question is usually not whether to fix something, but how to pay for it.

For many homeowners in Southeast Minnesota, the answer isn’t obvious. You might not have enough in savings to cover a big repair without wiping out your emergency fund. Credit cards feel risky when the balance starts climbing. And if you haven’t built up much equity in your home yet, a home equity loan might not even be on the table.

That’s where a personal loan can make a lot of sense. This guide walks through when a personal loan is a good fit for home improvements, how it compares to other options, and how to use one responsibly.

Yes, absolutely. Personal loans are flexible by design. Unlike a car loan or a mortgage, they are not tied to a specific purchase. Once you’re approved and funded, you can use the money for just about anything, including home repairs and renovations.

That makes them a practical option for projects like replacing a water heater, refinishing hardwood floors, upgrading a bathroom, fixing foundation issues, or replacing windows before winter. These are real, necessary expenses that protect your investment and your family’s comfort.

A personal loan for home projects is worth considering when one or more of these apply to your situation.

There is more than one way to fund your home projects. The most common solutions are personal loans and home equity loans. Both options can fund home improvements, but they work differently and serve different situations.

A home equity loan lets you borrow against the value you’ve built in your home. Because your home is used as collateral, lenders typically offer lower interest rates. However, you need to have enough equity to qualify, and the application process takes longer. If you fall behind on payments, your home is at risk.

A personal loan is unsecured, meaning it doesn’t use your home as collateral. Approval is based on your credit history and income, and you can often get funded faster. The trade-off is that rates may be slightly higher than a home equity loan, though still much more manageable than most credit cards.

For newer homeowners who are still building equity, a personal loan is often the more realistic and accessible choice.

Personal loan amounts vary by lender, but most range from a few hundred dollars to around $50,000. For smaller home repairs, this covers a lot of ground. A basic bathroom update, new flooring, HVAC repairs, or a fresh coat of exterior paint are all well within what a personal loan can handle.

Approval amounts depend on your credit score, income, and existing debt. Lenders want to see that you have the ability to repay comfortably, so they’ll look at your full financial picture before making an offer.

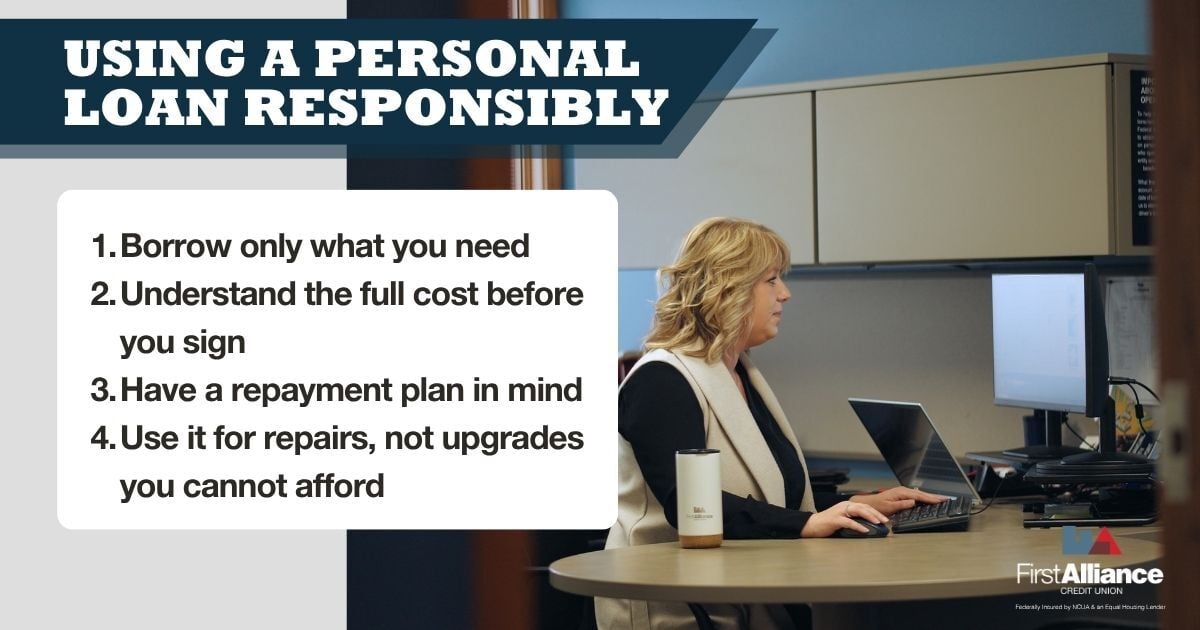

Getting approved is only part of the picture. Here’s how to make sure the loan for home repairs works in your favor.

Not every home project needs a loan. If the repair costs a few hundred dollars and you can cover it from your regular income or a small savings withdrawal without stressing your finances, that’s often the simpler path.

A personal loan makes the most sense when the cost is significant enough that paying out of pocket would either drain your savings or force you to put it off longer than you should. Think of it as a tool for bridging the gap between what you have and what you need, not a substitute for saving.

If you’re not sure whether a personal loan is the right fit, the easiest first step is to talk to someone at your financial institution before you apply. A loan advisor can help you look at your situation honestly, including your credit, your income, and how a new payment fits into your existing obligations.

At First Alliance Credit Union, you can have that conversation without any pressure or obligation. Whether you’re ready to apply or just trying to understand your options, the team there can help you think it through and find a path that works for your budget.

These are some of the most common questions homeowners have about using a personal loan for home improvement projects.

Yes. Personal loans are not tied to a specific purchase, so you can use the funds for repairs, renovations, or upgrades once you're approved and funded. It is a great tool for paying for small to medium sized home repairs.

It depends on your situation. A home equity loan may offer lower rates, but it requires sufficient equity and uses your home as collateral. A personal loan is faster, unsecured, and more accessible for newer homeowners still building equity.

The main advantages are predictable fixed payments, no collateral required, and fast funding. The trade-off is that interest rates can be slightly higher than secured options like a home equity loan. However, the interest rates on a personal loan are usually lower than with a credit card.

Most personal loans range from a few hundred dollars up to around $50,000, which covers most common repair and renovation projects. The amount you qualify for depends on your credit score, income, and existing debt.

If the cost is manageable from your regular income or savings without straining your finances, paying out of pocket is the simplest option. When the repair is urgent or the cost would deplete your emergency fund, a personal loan gives you predictable payments without touching your savings.

1 min read

If you go to a credit union or bank's website and search for information about loans, you'll immediately notice that most types of loans are...

1 min read

One of the biggest benefits of a personal loan is its flexibility. Unlike other types of loans, such as a mortgage or car loan, a personal loan can...

1 min read

One of the most versatile loans you can get from a financial institution is a personal loan. You can use the money for anything from funding your...