1 min read

Different Types of Mortgage Loans: A Simple Guide for Homebuyers

Buying a home is exciting. But the moment someone starts talking about types of mortgage loans, FHA financing, conventional vs FHA mortgage...

4 min read

Buying a home is one of the biggest financial decisions you’ll ever make. And somehow, the mortgage part of that decision often gets rushed.

People spend weeks thinking about kitchens, neighborhoods, and square footage. Then when it comes to choosing the loan, it suddenly feels overwhelming. So they default to whatever has the lowest rate and hope for the best.

If you’re wondering how to choose a mortgage that actually fits your situation, here’s the good news: it’s about much more than rate shopping. The right mortgage supports your job stability, your future plans, your comfort level, and how long you plan to stay in the home.

When the loan fits your life, it becomes a tool that works for you every single month.

Before comparing loan options, pause and ask yourself a few key questions:

These answers shape your mortgage decision more than any interest rate ever will.

If you’re planning to stay in your home for 15 to 20 years, it makes a lot of sense to lean toward long term stability. Knowing what your payment will look like year after year can bring real peace of mind.

On the other hand, if you see yourself relocating in five years or so, having a little more flexibility could work in your favor. Your plans, timeline, and comfort level all matter.

There isn’t one “best mortgage” that works for everyone. The right choice is the one that fits your life right now and supports where you’re headed next.

Once you understand your personal context, the loan types start to make more sense.

This is what most people picture when they think about a mortgage. Conventional loans typically require a credit score around 680 or higher and allow down payments as low as 3%. Stronger credit profiles are rewarded with better pricing, so this option works especially well if your credit is healthy and stable.

FHA stands for Federal Housing Administration. These loans are designed to be more flexible for buyers who may have experienced credit challenges in the past. At First Alliance, FHA loans are available down to a 640 credit score with a 3.5% down payment. Even if you have owned a home before, you can still use FHA as long as the property will be your primary residence.

If you have served in the military and have an honorable discharge with a Certificate of Eligibility, VA loans are one of the strongest options available. They require no down payment, offer very competitive interest rates, and do not require mortgage insurance. That last piece can significantly reduce your monthly payment.

USDA loans are built for buyers purchasing in eligible rural or smaller community areas. Like VA loans, they offer zero down payment options. For buyers still building savings, this can be the doorway into homeownership.

Each program exists for a reason. The goal is not to pick the most popular one. It is to pick the one that matches your credit profile, savings, and long term plans. Remember, the mortgage product that worked for your friend or co-worker, may not be the right fit for your situation.

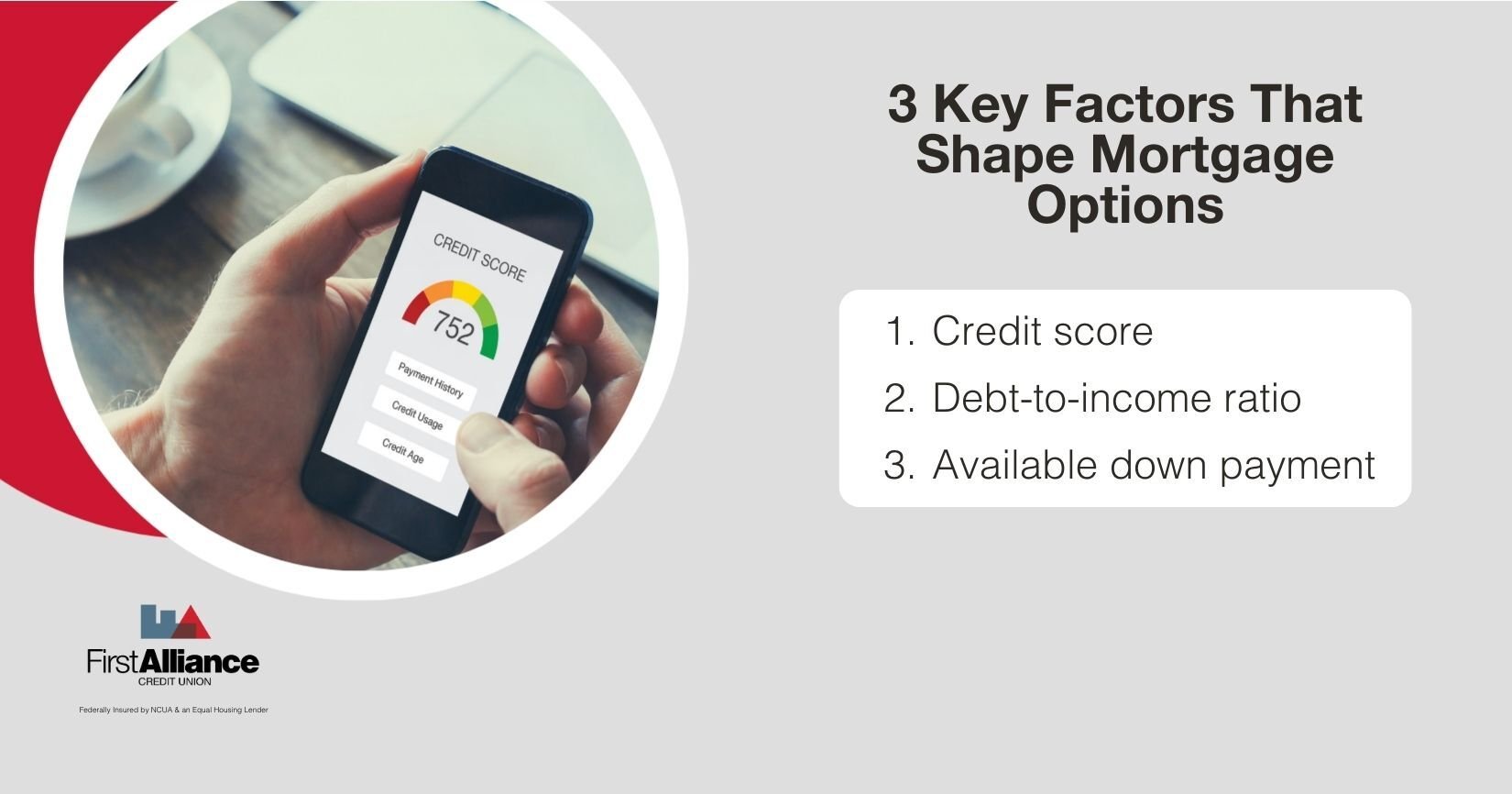

When you sit down with a lender, the conversation usually centers around three factors:

These are not barriers. They are guideposts that help narrow down which programs fit you best.

It is also smart to prepare for closing costs. In addition to your down payment, budgeting between $5,000 and $10,000 for appraisal fees, title work, taxes, and insurance is a practical move. Knowing this upfront prevents surprises and keeps you in control of the process.

This is where a lot of mortgage decisions really come down to personal preference.

A lower monthly payment can give you breathing room right now. But stretching payments over a longer period usually means paying more interest over time.

A higher monthly payment might feel like a stretch, but it could mean saving a significant amount in interest and owning your home much sooner.

For example:

A 30 year fixed mortgage spreads payments out and keeps them lower month to month. That stability and flexibility are why it’s so popular.

A 15 year fixed mortgage typically comes with a lower interest rate and much less interest paid over the life of the loan. The payment is higher, but you build equity faster and become mortgage free sooner.

Neither choice is automatically better. It depends on what matters more to you, lower monthly obligation or faster long term payoff.

If you’ve heard about adjustable rate mortgages and felt unsure, that’s normal.

An adjustable rate mortgage, often called an ARM, starts with a fixed rate for a certain number of years. After that, the rate can change based on the market.

This can be a smart move if you know you will not stay in the home long term. Maybe you are in a temporary job. Maybe you plan to move in five years. In those cases, locking into a 30 year structure may not be necessary.

But if you value predictability and want your payment to stay consistent for decades, a fixed rate may feel more comfortable.

When it comes to the fixed vs adjustable mortgage decision, it really comes down to your timeline and your tolerance for change.

If you’re trying to figure out how to choose a mortgage and everything feels overwhelming, simplify it.

You don’t have to know all the answers before talking to someone. In fact, most clarity comes through conversations with professionals who can guide you through the mortgage process.

Mortgages are not just math. They are about your life, your stress level, your future goals.

A good lender will ask about more than your credit score. They will ask about your plans. Your comfort level. Your bigger financial picture.

At First Alliance, our local home lending team takes the time to understand what you are trying to accomplish. We also offer credit and financial guidance if you want to strengthen your position before making a move.

We will help you find a mortgage that fits your life, not force you into one.

If you’re ready to explore your options or just want to talk through what makes sense for you, reach out. We’re here to walk through it with you.

1 min read

Buying a home is exciting. But the moment someone starts talking about types of mortgage loans, FHA financing, conventional vs FHA mortgage...

1 min read

If you're considering purchasing a home, you will need to plan for a having down payment. While saving up for a down payment is a popular choice,...

1 min read

If you're in the process of buying a home, you’ve likely come across the term Private Mortgage Insurance (PMI). It’s one of those extra costs that...