Kamel LoveJoy

Kamel LoveJoy

1 min read

How to Use Home Equity: Smart Strategies for Savvy Homeowners

Home Equity 101: A Quick, No-Jargon Refresher Home equity is the portion of your home you own rather than owe. Every mortgage payment you make and...

Every morning, Jose opens his small protein restaurant and flips the first batch of protein waffles while his wife texts photos of his grandmother and parents getting ready for the day. He is from Lima, Peru, in love with his wife, and devoted to caring for his grandmother and parents. With a new baby on the way, he needs more space and maybe a yard.

For nearly a decade, Jose rented apartments that never felt like home. He paid taxes every year with his ITIN and kept careful records, but each time he asked about buying a house, he heard the same reply: you need a Social Security Number.

Everything changed when a regular at the restaurant told him about First Alliance Credit Union’s ITIN Home Loan. Jose expected another polite no. Instead, he found a team ready to listen and a real plan.

An ITIN Home Loan is a mortgage for people who file U.S. taxes using an Individual Taxpayer Identification Number (ITIN). It works like any other home loan. Lenders review income, credit, identification, assets, and the property to confirm the payments are affordable and sustainable.

To qualify, Jose needed to show:

Two years of ITIN tax returns

Verifiable income from his protein restaurant

Acceptable identification

Credit history or alternative credit such as on time rent and utility payments

A safe debt to income (DTI) ratio

The First Alliance team helped him organize everything without judgment.

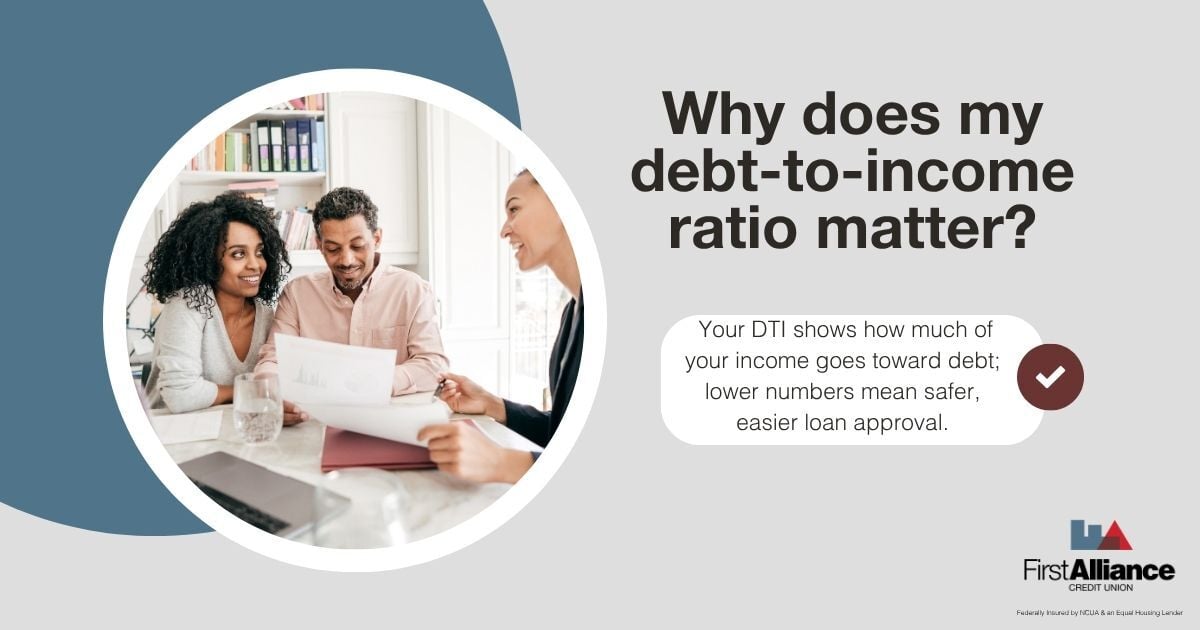

At the first meeting, Jose’s loan officer wrote a simple equation for Debt to Income Ratio (DTI):

DTI = Total Monthly Debt Payments ÷ Total Gross Monthly Income

Example

If monthly debts are $1,500 and gross income is $5,000, DTI is 30%.

Most lenders prefer DTI below 43%. Lower is better because it leaves room for real life.

Why DTI matters

DTI is not just a bank number. It is a budget safety check. A lower DTI means money is left for groceries, gas, childcare, home repairs, and savings. It protects your household from stress and missed payments.

How First Alliance helped Jose lower his DTI

They showed how paying off a small personal loan would drop his DTI by several points.

Because Jose is self employed, they explained how underwriters view business income and which expenses reduce qualifying income. They helped him prepare a clean year to date profit and loss statement and match it to bank deposits.

They consolidated one balance to reduce monthly obligations and set a realistic budget that works even with childcare and family support.

Jose left with clear targets and a plan he could follow.

Jose keeps his receipts and schedules, but the team helped him package his file so underwriting would move faster.

Most lenders require

Government issued photo ID and ITIN documentation

Two years of federal tax returns filed with an ITIN

Self employed income: year to date profit and loss, last two years business returns if applicable, 2 to 3 months of business and personal bank statements that show deposits

If W2 in addition to self employment: recent pay stubs

Rental history showing on time payments

If you do not have traditional credit, you can show alternative credit, 12 months of rent, utilities, or insurance payments on time. Jose brought his rent receipts and utility bills.

Use rent to build credit: Pay rent electronically each month, save the confirmations, and ask your landlord for a signed rental verification or ledger showing 12 months of on time payments. You can also enroll in a reputable rent reporting service that sends your payment history to the major credit bureaus so lenders can see it during pre approval.

When Jose’s DTI moved into a comfortable range, he needed to know what price made sense for his budget and his growing family. Instead of guessing, his lender showed him First Alliance Credit Union’s How Much Can You Afford Calculator.

The calculator helped Jose see:

How income, debts, and DTI shape affordability

What a monthly payment might look like at different prices

How a slightly larger down payment or lower debt could expand his safe range

With a clear affordability number, Jose and his wife focused on homes that fit their budget and the yard they hoped for.

The team stayed close.

They explained why each document mattered and how it speeds up underwriting.

When the file moved to underwriting, they prepared Jose for common conditions like updated bank statements or a letter explaining a large deposit.

When his pre-approval arrived, they walked him through next steps so he could shop with confidence.

They also connected Jose with Three Rivers Community Action for a homebuyer class. He left with a plan for emergency savings, utilities, and the first repair fund so life with a newborn would be easier.

Press play for Chelsy's quick tips on the types of loans available.

Jose’s steps were clear:

Pre-qualification based on shared info

Pre-approval with document verification

Home search and offer with the pre approval letter

Underwriting and clearing conditions

Closing and keys

What lenders look for the whole way: reliable income, complete documents, a safe DTI, and quick responses.

When a seller accepted their offer on a house with a small yard, Jose was ready.

Typical closing costs

Appraisal

Title search and title insurance

Recording and transfer fees

Lender fees if applicable

Prepaid taxes and homeowner insurance

Plan for 2 to 5% of the price. You will receive a Loan Estimate early and a Closing Disclosure before signing so every dollar is clear. Jose reviewed both and asked questions until he felt completely comfortable.

He called his wife from the driveway after closing. They had keys, a quiet street, and space for a stroller.

Ready to buy with an ITIN? Start with clarity, not guesswork. Use the How Much Home Can You Afford calculator to see a payment and price range that truly fits your budget. Then meet with a lender who will review your debt to income ratio, explain exactly which documents to gather, and map out your fastest path to pre-approval. Visit First Alliance Credit Union for one-on-one guidance and a clear plan from first question to keys.

1 min read

Home Equity 101: A Quick, No-Jargon Refresher Home equity is the portion of your home you own rather than owe. Every mortgage payment you make and...

1 min read

Maya is tired of rising rent. She finds a clean two-bedroom manufactured home in a well-run park near work. The price fits her budget. She needs a...

1 min read

When you buy a house, you’re not just getting a nice place to call your own. You’re also buying one of the few assets that tends to increase in value...