Kamel LoveJoy

Kamel LoveJoy

1 min read

Back-to-School Budgeting Basics

As the new school year approaches, the excitement of preparing your kids for another year of learning is often accompanied by financial stress. On...

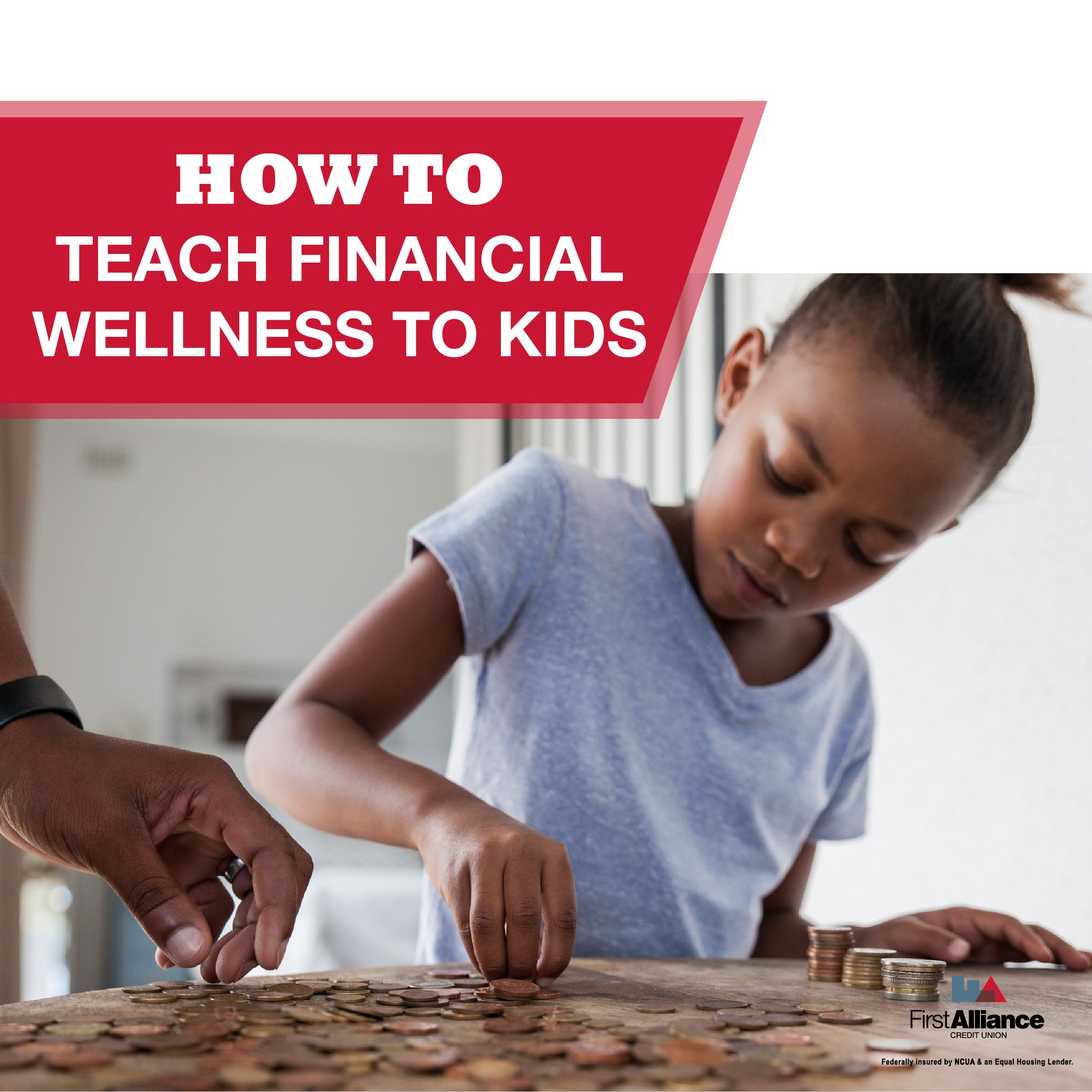

As parents, teaching kids financial responsibility is crucial. But when it comes to allowances, should you give them cash for chores or set them up with a kids' debit card? Let’s meet Mike and Sarah, who are in this exact dilemma with their 13-year-old daughter, Lily. Mike thinks cash is simpler, while Sarah believes a debit card like the one First Alliance Credit Union offers through Greenlight might teach Lily valuable money management skills. Here’s what they learned in their quest to find the best option.

Traditional Allowance (Cash):Most people agree that allowances help build healthy habits early. Handing out a cash allowance is straightforward. Lily would complete her chores, and at the end of the week, she’d get her cash—simple, tangible, and quick. Mike argues that cash allows Lily to see the value of money physically and understand how quickly it can be spent. However, in an increasingly digital world, cash can feel a bit limiting.

Kids’ Debit Cards: Debit cards for children, like Greenlight, offer more than just digital spending. These cards are packed with features that teach financial literacy, from budgeting to saving and investing. Sarah loves that Lily would have a “real-world” money experience while still allowing her to keep an eye on Lily’s spending through parental controls in the app.

So, which option is better? Let’s break it down.

With Greenlight, Lily would get her own debit card, and Sarah and Mike could set parental controls on the app. Here are the key benefits they considered:

Money Management Skills: The Greenlight app lets kids split money into “Spend,” “Save,” and “Give” categories. This setup helps Lily practice budgeting by dividing her allowance across different goals—whether that’s buying new headphones, saving for a bigger purchase, or donating.

Digital Convenience: With a debit card, Lily could make purchases online, especially as many stores are going cashless. Sarah liked that Lily wouldn’t need cash to buy things or worry about losing it, thanks to security features that allow Sarah to freeze or cancel the card if it’s misplaced.

Real-Time Tracking: Sarah and Mike would get notifications every time Lily makes a purchase, and Lily can see where her money goes. Sarah and Mike can also approve where their child spends money, if their child wants to buy something over budget, they can send you a picture of it. This visibility helps Lilly understand spending habits and makes budgeting easier for everyone involved.

Parent-Paid Interest: Another unique feature with Greenlight is the Parent-Paid Interest, where Sarah and Mike can reward Lily’s savings by adding a small interest amount. It’s a hands-on way for Lily to see her money grow faster than stuffing it in a piggy bank.

While Sarah was sold on the debit card, Mike brought up some strong points in favor of cash.

Tangible Experience: Cash gives a sense of weight and value—literally. Lily might better understand spending limits when she physically hands over bills and sees her wallet empty. It’s a concrete way to learn money has limits, which can be hard to grasp with a card.

Less Risk of Overspending: With cash, Lily can only spend what she has, avoiding accidental overspending that might happen with a card. Cash allowance doesn’t come with potential fees or the risk of Lily “swiping” away her savings too quickly.

Simplicity: Let’s be honest; setting up an allowance with cash can be simpler for busy families. It doesn’t require apps, accounts, or devices—just a weekly payout and a list of chores.

Whether Lily gets a debit card or cash, she’ll learn financial basics, but each method emphasizes different skills.

With Cash: Lily would understand budgeting in a simple way, learning to count her money and divide it mentally between wants and needs. Cash also makes it easier to see the effects of impulse purchases—once it’s spent, it’s gone.

With a Debit Card: Greenlight’s app would allow Lily to set specific savings goals and track her progress, helping her see the power of planning and delayed gratification. Plus, if she wants to learn to invest, Greenlight’s platform can introduce her to investing in a kid-friendly, supervised way. Sarah likes the idea of her learning to grow her money instead of only spending it.

Parental control is another crucial consideration. Cash means freedom but can lack oversight, while a debit card with an app provides ongoing visibility into Lily’s spending.

Debit Card Monitoring: With Greenlight, Sarah and Mike could see where Lily spends and set spending limits. They’d also be able to receive alerts if she spends more than they think is wise, helping to teach responsible spending gently.

Cash’s Freedom: Cash allows Lily a bit more autonomy, which could be beneficial as she matures. Mike argues that while monitoring is helpful, at some point, it’s important for Lily to learn how to spend wisely without relying on tech.

Debit cards for kids can come with fees, depending on the plan. Greenlight, for instance, offers different tiers with various features. Sarah thinks the fee is worth the convenience and teaching benefits, but Mike isn’t as sure.

Cash, on the other hand, is free to use, with no monthly fees or hidden costs. If you want the basics, cash is a low-cost option. But if you see value in a structured financial learning experience, the cost of a kids' debit card could be a worthwhile investment.

Choosing between cash and a debit card also depends on a child’s age and maturity. For younger children, cash might be a better fit because it’s simpler and doesn’t require managing accounts or apps.

However, as kids enter their teens, they’re likely ready for a debit card. At 13, Lily is exploring her independence, so having her own card could be a smart way to build her confidence in managing money before she’s old enough for a traditional bank account.

In the end, Sarah and Mike decided on a hybrid approach: Lily would get a small cash allowance to spend as she likes but also receive a portion of her allowance on a Greenlight debit card. The cash helps her with tangible spending lessons, while her card lets her set savings goals, learn to invest, and learn how to handle money digitally.

This way, she gets the freedom of cash with the budgeting power of a debit card—and everyone’s happy!

When it comes to Kids’ Debit Cards vs. Traditional Allowance, there’s no one-size-fits-all answer. For Sarah and Mike, a hybrid solution worked best, balancing independence with oversight. Whether you go cash, card, or both, the key is open conversations and real-world experiences that prepare kids for financial independence. With tools like Greenlight and a partner like First Alliance Credit Union, teaching kids about money has never been easier—or more impactful.

*First Alliance Credit Union members are eligible for the Greenlight SELECT plan at no cost when they connect their First Alliance Credit Union account as the Greenlight funding source for the entirety of the promotion. Subject to minimum balance requirements and identity verification. Upgrades will result in additional fees. Upon termination of promotion, customers will be responsible for associated monthly fees. See terms for details. Offer ends 10/15/2026. Offer subject to change and partner participation.

1 min read

As the new school year approaches, the excitement of preparing your kids for another year of learning is often accompanied by financial stress. On...

1 min read

Practical money management skills learned at an early age can have a lasting impact on the rest of your child’s life. In fact, this is one of the...

1 min read

Most parents don’t sit down and formally teach their kids about money. It tends to happen in passing, at the grocery store, in the car, or when a...