Jenna Taubel

Jenna Taubel

1 min read

Refinance a Loan: Discover the Benefits

Imagine this: A young couple, Jamie and Alex, bought their first car two years ago. They were excited about their new ride but soon realized they...

Refinancing a loan means transferring your existing debt to a new lender, often to benefit from a better interest rate, more manageable payments, or to free up funds for your other financial priorities. Many people choose to refinance to lower their monthly payments, reduce the long-term cost of borrowing, or access cash for important personal goals. By finding a loan with improved terms, you can save money over the life of your loan and create more room in your budget for what matters most to you and your family.

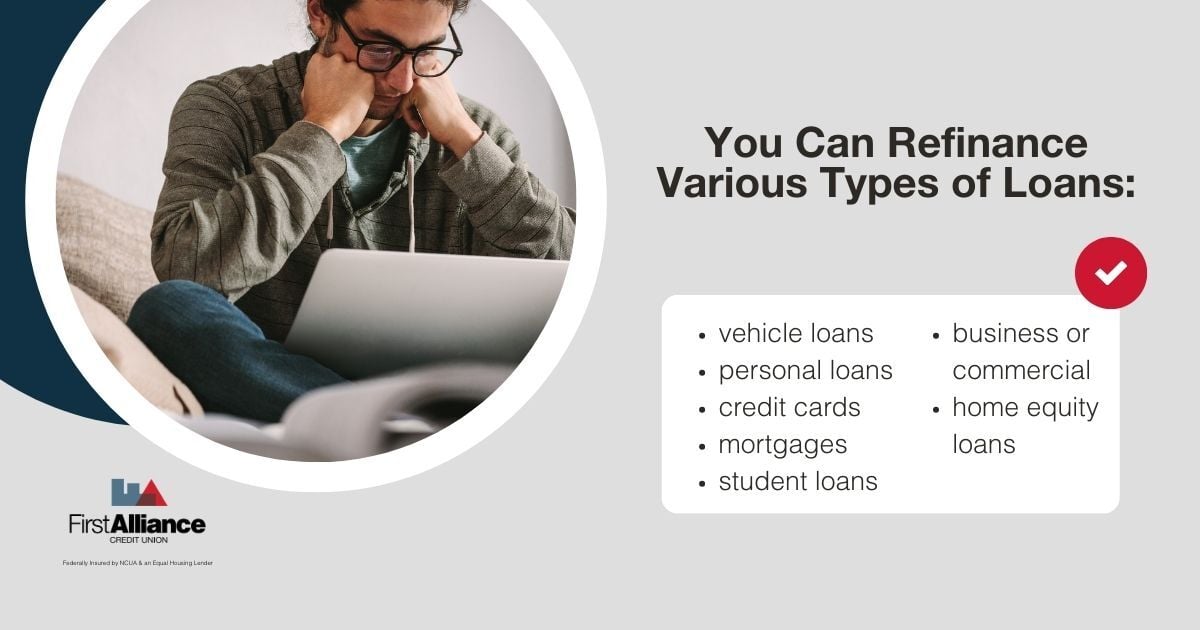

You can refinance almost any loan or line of credit, this means whether you’re looking to lower the rate on your auto loan, restructure your mortgage to reduce monthly payments, streamline debt by consolidating credit cards, or address other financial needs, refinancing could be an option.

You can refinance various types of loans:

Each type of loan may have its own benefits and considerations when it comes to refinancing, allowing you to find the solution that best aligns with your current goals and financial well-being. However, there are exceptions due to certain regulations and lender offerings.

For instance, some lenders do not handle student loans, or in the case of federal student loans, they are often subject to government rules that can limit your ability to refinance them through a traditional lender. In addition, some credit unions and banks may not offer refinancing for specific types of real estate loans or investment properties.

It may be a good time to consider refinancing your loan if your financial circumstances, goals, or the market itself have changed since you first borrowed. Common reasons to refinance include securing a lower interest rate, reducing monthly payments to better fit your budget, shortening the loan term to pay off debt faster, or converting from a variable to a fixed rate for more predictable payments.

Market conditions play a significant role in determining the best time to refinance. Interest rates fluctuate based on economic factors, so keeping an eye on these changes can help you identify optimal refinancing opportunities.

As Jordan Kaehler, Loan Portfolio Manager at First Alliance Credit Union, advised on a recent Good Money Moves podcast episode:

"If you hear any buzz about the Fed reducing rates, shop around. See who's offering what rates and what would be the best for you." ~ Kaehler

For example, if you initially financed your vehicle during a period of high interest rates, you could benefit significantly from refinancing when rates drop. You might also consider refinancing if your credit score has improved, giving you access to better loan offers, or if you need to tap into your home or asset equity for large expenses such as home improvements, education costs, or consolidating high-interest debt.

Most importantly, refinancing can help you create more financial flexibility, ensuring your borrowing stays aligned with your current lifestyle and future goals. Before making a decision, it’s smart to review your overall financial picture, compare available options, and think about how refinancing could impact your long-term plans.

The refinancing process may seem daunting, but it generally involves a few straightforward steps no matter what type of debt your seeking to refinance:

Determine your current loan balance and interest rate, these two numbers are your starting points when considering refinancing. To find this information, look to the most recent statement from your lender or log in to your online account to find your outstanding principal and the current rate you’re paying. Having this information ready not only allows you to see how much you still owe, but it also helps you accurately compare new loan offers side by side.

Take the time to compare offers from a variety of financial institutions, including credit unions, banks, and online lenders, to ensure you’re getting the most favorable terms. Carefully review details like the Annual Percentage Rate (APR), which represents the true cost of borrowing by factoring in both the interest rate and any lender-associated fees. Even small differences in APR can add up to significant savings over the life of your loan. By shopping around, you put yourself in the best position to secure a loan that truly supports your financial goals and helps you maximize the benefits of refinancing a loan.

Once you’ve identified a refinancing offer that aligns with your goals, it’s time to complete your application. Be prepared to provide essential documentation, which typically includes:

You may also be asked to provide identification or additional supporting documents, like the vehicle title if your refinancing an auto loan, to help the lender assess your loan eligibility. Submitting accurate and up-to-date information ensures the process moves smoothly and helps you secure the best possible terms.

Once your refinancing application is approved, your new lender will typically handle paying off your existing loan directly, taking care of all the necessary payoff procedures with your current lender. From there, you’ll transition to making payments according to your new loan agreement.

It’s important to carefully review all loan documents, including the terms, interest rate, payment schedule, and any applicable fees, before signing. This ensures there are no unexpected changes or obligations, and that your new loan truly aligns with your financial goals. Don’t hesitate to ask questions or seek clarification from your lender if anything is unclear, your peace of mind and financial confidence are worth it.

Hit play to explore the benefits of refinancing a loan and how to start the process.

Refinancing can have both positive and negative impacts on your credit score. Initially, you might see a reduction in your score by three to five points due to new credit inquiries during the refinancing process.

However, as Kaehler noted in the recent podcast:

"Typically, you might see a short-term dip in your credit score after applying and closing the loan. However, it's going to rebound relatively quickly with positive payment history." ~ Kaehler

However, one significant benefit of refinancing, particularly for credit card debt, is the potential for substantial credit score improvement. By moving high-interest credit card debt to an personal loan with a lower interest rate, you can reduce your credit utilization rate, which can positively impact your credit score.

Kaehler explained how this works on the podcast,

"If you free up your credit card balances and move it to installment debt, you're freeing up that utilization, which can lead to a higher credit score." ~ Kaehler

Refinancing a loan is a significant financial decision, and choosing the right lender is crucial. First Alliance Credit Union offers a compassionate, down-to-earth, and trustworthy approach to refinancing. With a commitment to providing transparent and competitive rates, First Alliance ensures that you receive the best possible terms for your financial situation.

Refinancing a loan can be a powerful tool to save money, improve your credit score, and achieve greater financial flexibility. By understanding the process and working with a trusted lender like First Alliance Credit Union, you can navigate the refinancing journey with confidence and ease.

1 min read

Imagine this: A young couple, Jamie and Alex, bought their first car two years ago. They were excited about their new ride but soon realized they...

1 min read

Bailey still remembers easing her silver hatchback off a Rochester dealer’s lot—heart pounding, paperwork piling, and a monthly payment that felt...

1 min read

If your debt levels are becoming burdensome and you’re struggling to make monthly payments it might be time to consider either refinancing your debt...