Jenna Taubel

Jenna Taubel

1 min read

5 Easy Steps To Financial Literacy For Beginners

Did you know that, according to one report, almost half of Americans make a New Year’s Resolution related to finance? If you’re one of those people,...

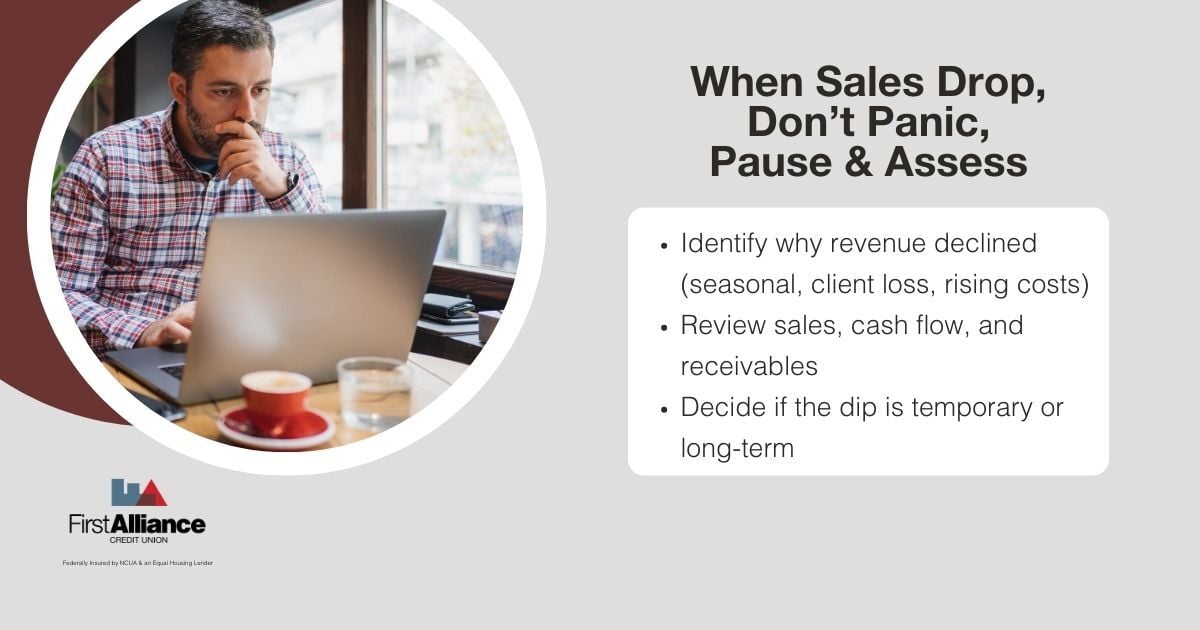

Unexpected dips in sales happen, even to healthy, well-run small businesses. A seasonal slowdown lasts longer than you expected. A major client pauses or cuts back their spending. Costs rise faster than revenue. Or broader economic and political uncertainty starts to ripple through your market.

When sales revenue drops suddenly, it can feel overwhelming and frustrating, but the right moves early can help you protect cash flow, stabilize operations, and avoid long-term damage.

Here’s a step-by-step guide for small business owners to follow when revenue declines, and how to get the right financial support before the stress starts to pile up.

A revenue drop doesn’t automatically mean your business is failing. The first step is understanding what kind of dip you’re facing and how serious it really is. Are you seeing a short-term fluctuation, a predictable seasonal slowdown, or the early signs of a structural shift in your market or business model?

Assess the revenue problem by asking yourself:

Pull your recent sales reports, cash flow statements, and receivables. Even a simple snapshot of where money is coming in and going out can help you move from reacting under stress to making confident, strategic decisions.

Once you define the nature of the decline, how steep it is, how long it’s lasted or expected to last, and what’s driving it, you can respond with a clear plan instead of reacting on instinct.

Cash flow—not profit—is what keeps the doors open. You can have a strong business on paper and still struggle to pay your team, cover rent, or keep up with vendor bills if cash isn’t actually coming in when you need it. In a downturn, your first priority is making sure there’s enough money moving through the business week by week to cover essential expenses and keep operations running.

Quick actions to consider when your sales decline quickly:

Small, thoughtful adjustments now can buy you time, protect your cash flow, and ease the pressure while you map out your next steps.

One of the biggest mistakes business owners make during a downturn is waiting too long to ask for help. If you work with a local credit union or community-focused financial institution, start the conversation early. Don’t wait until you’ve missed a payment, drained your reserves, or felt forced into a last-minute decision.

Share what you’re seeing in your numbers, how long you expect the slowdown to last, and what you’re already doing to adjust. The more proactive and transparent you are, the easier it is for a trusted financial partner to walk alongside you, talk through options, and help you find solutions that protect both your business and your long-term goals.

Early communication with lenders can open doors to:

Lenders have more options to support you through periods of slower sales when they understand what’s happening before payments are missed and stress starts to snowball.

While cutting costs helps, revenue recovery is just as important. Once you’ve stabilized your cash flow, shift some of your focus toward rebuilding sales so you’re not just surviving the slowdown, but positioning your business to grow again when conditions improve.

Consider simple sales growth tactics such as:

Sometimes small shifts in marketing strategies can create meaningful impact for small business when sales have declined, especially when paired with the right financial support.

Short-term cash flow challenges don’t always require drastic measures. The right, well-structured financing tool can help you bridge a rough patch, protect your day-to-day operations, and avoid creating unnecessary long-term strain on your business.

Short-term loan options to cover lost revenue may include:

The key is choosing a solution that fits your situation, not a one-size-fits-all product. The best option for your business will depend on factors like how quickly revenue dropped, how predictable the recovery timeline is, what your existing debt obligations look like, and how much flexibility you need in monthly payments.

For some businesses, a small line of credit that can be drawn on and paid down as needed makes the most sense. For others, a short-term working capital loan with a clear payoff plan provides more stability. In some cases, restructuring existing debt to lower monthly payments can free up just enough cash to get through a slow period without sacrificing growth opportunities.

The goal isn’t to take on more financing just for the sake of it, it’s to match the right tool to the specific challenge you’re facing so you can steady your cash flow today while still protecting your long-term financial health.

Running a business is hard enough without navigating uncertainty in isolation. Having a financial partner who understands small businesses, and your local market, can make a real difference.

At First Alliance Credit Union, we work with small business owners every day who are facing unexpected challenges. If your revenue has dropped and you’re not sure what your next move should be, our team can help you:

You don’t have to have all the answers, we’ll help you think through them.

Reach out to First Alliance Credit Union today to talk with a real person who’s ready to support your business, your goals, and your next chapter. Because when times get tough, the right financial partner doesn’t disappear, they show up.

1 min read

Did you know that, according to one report, almost half of Americans make a New Year’s Resolution related to finance? If you’re one of those people,...

1 min read

How exactly do you get your finances where you want them? Everyone's situations and goals are a little bit different, but these two financial health...

1 min read

Managing your money goes beyond keeping tidy records or color-coding spreadsheets. When your finances become disorganized, the real impact shows up...