1 min read

Understanding the Overdraft Line of Credit: A Lifeline for Families

Imagine you've just bought a cozy new home for your family. It’s the perfect spot—big enough for your growing kids and close enough to work to avoid...

5 min read

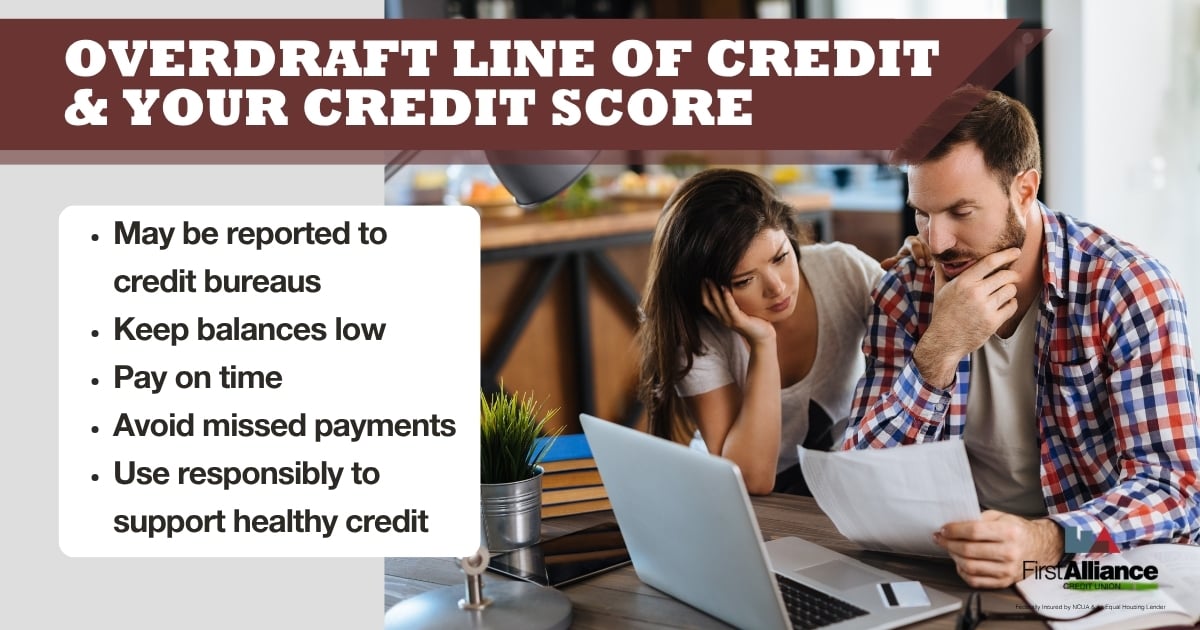

Does an overdraft line of credit affect your credit score? Yes, but not in the way most people expect. Because an overdraft line of credit is an actual credit product, it can appear on your credit report and influence your score through the same factors as any other credit account: your balance, your credit utilization, and whether you pay on time. Simply having the line of credit in place is not the concern. How you use and repay it is what matters.

Yes, it can. An overdraft line of credit works similarly to a personal line of credit or credit card. When you open one, your credit union may run a credit check, and the account itself, including your credit limit, balance, and payment history, may be reported to the credit bureaus.

That's different from basic overdraft fees or Courtesy Pay services, which draws from your own checking account, often bringing you further negative until you add new funds. Occasional overdrafts handled this way typically won't show up on your credit report.

Using your overdraft line of credit to cover a short-term gap will not automatically hurt your score. What matters is how the balance is managed afterward. If you draw on the line and repay it in a reasonable time, it can be a neutral or even a positive mark on your credit history, since it shows a lender that you can manage credit responsibly.

Where it can work against you is if the balance grows large relative to your credit limit, since credit utilization is a real factor in your score, or if the amount sits unpaid for an extended period. Treating your overdraft line of credit the way you would treat a credit card, meaning borrow what you need and pay it down promptly, keeps it working in your favor rather than against you.

Yes. Because this is a reported credit account, a missed or late payment can be reported to the credit bureaus and may lower your score, the same as a missed payment on a credit card or personal loan would. If a balance goes unpaid long enough, it can also be sent to collections, which stays on your credit report for up to seven years.

This is the most important thing to understand about how overdraft line of credit works. The tool itself is not risky. An unpaid balance is. Setting up low-balance alerts and payment reminders through mobile or online banking is one of the simplest ways to stay ahead of this.

Repayment terms vary by financial institution, but most overdraft lines of credit are repaid in one of these ways:

Interest typically applies to the amount you borrow until it is repaid, so paying down the balance sooner reduces what it costs you. Your specific rate, credit limit, and repayment schedule depend on your individual account and creditworthiness, which is why we do not publish one-size-fits-all numbers here.

Choosing the right overdraft protection option depends on your habits, your comfort with credit, and how much of a cushion you already have. Here is how the three compare.

| Feature | Overdraft Line of Credit | Linked Savings Transfer | Courtesy Pay |

| How it covers a shortfall | Draws from an approved credit line up to your limit | Pulls from your own savings account | Bank covers the transaction based on account standing |

|

Cost |

Interest on the amount borrowed | Typically no fees or charges, since it is your own money | Flat fee per item, no interest |

| Credit report impact | May appear on your credit report as a credit account | No credit impact | Does not appear on your credit report |

| Repayment required | Yes, balance must be repaid over time | No, your are using your own funds | No, it is a one-time fee per transaction |

| Best for | Members comfortable managing a small credit balance responsibly | Members who keep a savings cushion and want the lowest-cost option | Members who need occasional coverage and prefer a predictable fee |

None of these is automatically the right answer for everyone. It comes down to whether you would rather use your own money, use a small line of credit and manage it like a credit account, or accept a flat fee now and then.

Say your car insurance payment is scheduled for the 28th, but payday is not until the 1st. If you have an overdraft line of credit set up, it can cover that gap so your payment goes through without a decline. You will owe that amount back, plus any applicable interest, but your insurance stays current and your account stays in good standing. Once your paycheck lands, you repay the balance and you are back to zero. Handled that way, it is a tool doing exactly what it was designed to do.

It depends on what you value most. If you are comfortable managing a small credit balance and want flexibility beyond your own savings, an overdraft line of credit can be a smart option, and responsible use can even support your credit history over time. If you would rather avoid interest and credit reporting altogether, a linked savings transfer may fit better. If you only need occasional coverage and prefer a flat fee with no credit involved, Courtesy Pay may be the simplest choice.

The best move is comparing all three against your own spending patterns and comfort level. If you would like help figuring out which overdraft protection option fits your life, schedule a quick conversation with a First Alliance team member. We are here to help you choose!

Here are quick answers to the questions members ask us most often about overdraft lines of credit and credit scores.

Not on its own. Courtesy Pay and linked savings transfers generally do not involve credit reporting. An overdraft line of credit is a credit account, so it can affect your score, mainly through how you manage the balance and whether payments are made on time.

Often, yes. Because it is a credit product, your credit union may review your credit history when you apply, similar to applying for a small line of credit or credit card.

Repayment terms vary by account, but most are structured with manageable minimum payments or automatic repayment from incoming deposits.

Yes. Many members combine a linked savings account with a small overdraft line of credit for extra flexibility. Talk to us about what setup works best for your account.

Overdraft protection exists because cash flow gaps happen to everyone, even careful budgeters. Understanding how your overdraft line of credit works, and staying ahead of repayment, is the difference between a helpful safety net and a source of stress.

If you have questions about your current overdraft protection setup, or you want to explore whether an overdraft line of credit is right for you, our team at First Alliance Credit Union is ready to talk it through!

1 min read

Imagine you've just bought a cozy new home for your family. It’s the perfect spot—big enough for your growing kids and close enough to work to avoid...

1 min read

When money timing gets tight, overdraft protection keeps essentials paid without panic. This guide helps you pick the setup that fits your habits,...

1 min read

Nobody likes overdrawing their account. While you might feel embarrassed about spending money you didn’t have, or using the wrong account for an...