Jenna Taubel

Jenna Taubel

1 min read

What is an Educational Credit Score?

You hear about apps and websites offering free credit scores all the time these days, which is great! These educational credit scores allow regular...

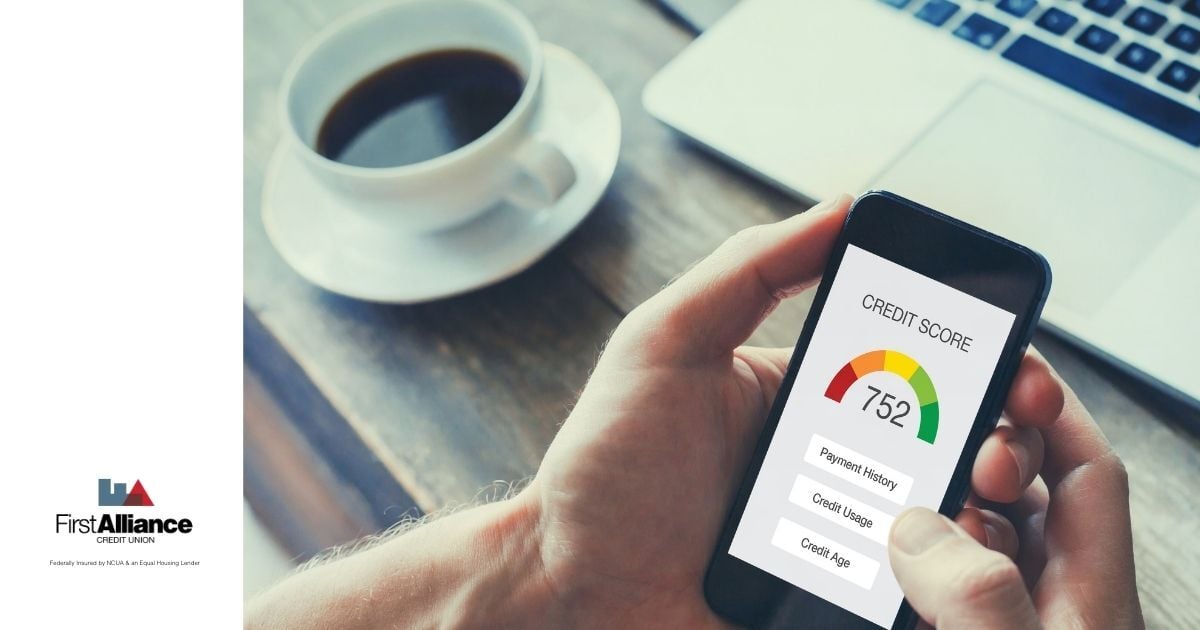

If you’ve ever applied for a loan, credit card, apartment, or even a job, you’ve likely heard the terms soft credit check and hard credit pull. While both involve reviewing your credit information, they serve very different purposes and affect your credit score in different ways. Understanding the difference can help you protect your credit and make more confident financial decisions.

A soft credit check (also called a soft inquiry) is a review of your credit report that does not affect your credit score. These checks are typically used for informational or pre-approval purposes, such as helping lenders estimate your eligibility or potential rates without requiring a full application. Because a soft inquiry isn’t tied to a specific request for new credit, it’s considered a low-risk review of your credit profile. That means you can explore your options, stay informed about your credit health, and receive personalized offers without worrying about lowering your score.

Soft inquiries are visible only to you on your credit report. Lenders do not see them when evaluating a credit application.

A hard credit pull (or hard inquiry) occurs when a lender reviews your credit as part of a formal credit application. This type of inquiry signals that you’re actively seeking new credit and allows the lender to look closely at your full credit history, including your payment track record, existing debts, and how much credit you’re already using. Because it’s tied to a specific application for new credit, it shows up on your credit report as a sign that you may be taking on additional financial obligations.

Hard inquiries can temporarily lower your credit score, usually by a few points. They remain on your credit report for up to two years, though their impact typically fades after the first year.

Here’s a quick comparison chart to highlight the key similarities and differences between these two types of credit checks.

| Feature | Soft Credit Check | Hard Credit Pull |

|---|---|---|

| Affects credit score? | ❌ No | ✅ Yes (slight, temporary) |

| Requires your permission? | ❌ Not always | ✅ Yes |

| Visible to lenders? | ❌ No | ✅ Yes |

| Used for applications? | ❌ No | ✅ Yes |

| Stays on credit report? | Yes (visible only to you) | Yes (up to 2 years) |

Both soft and hard inquiries are recorded by the major credit bureaus, Experian, Equifax, and TransUnion, but they’re treated very differently in credit scoring models. Only hard inquiries are factored into your score, and even then, they’re just one small piece of the overall picture. Soft inquiries never influence your score, so you can check your own credit or explore prequalification offers without worrying about lowering it.

Knowing whether a lender uses a soft check or a hard pull helps you:

Most lenders offer prequalification using a soft credit check, allowing you to explore options before committing to a full loan application.

Soft credit checks help you stay informed. Hard credit pulls help lenders make confident lending decisions. Neither is inherently “bad.” What matters is understanding when and why each is used so you can protect your credit and plan ahead. Before applying for credit, always ask:

Asking this question can help you protect your credit and stay financially confident.

If you’d like help understanding your credit or exploring options that won’t hurt your score, the team at First Alliance Credit Union is here for you. Contact us to review your situation and walk through the right next steps together.

1 min read

You hear about apps and websites offering free credit scores all the time these days, which is great! These educational credit scores allow regular...

1 min read

Credit cards are an important financial tool. However, many people who have a poor credit history or no credit history cannot qualify for a typical...

1 min read

Not having a credit score isn't necessarily a bad thing. We all have to start somewhere. Building credit history is important, especially as you...