Kamel LoveJoy

Kamel LoveJoy

1 min read

How To Choose a Credit Card

Credit cards are a big responsibility. If you are thinking about getting a credit card, make sure it's the right one for you. While credit cards can...

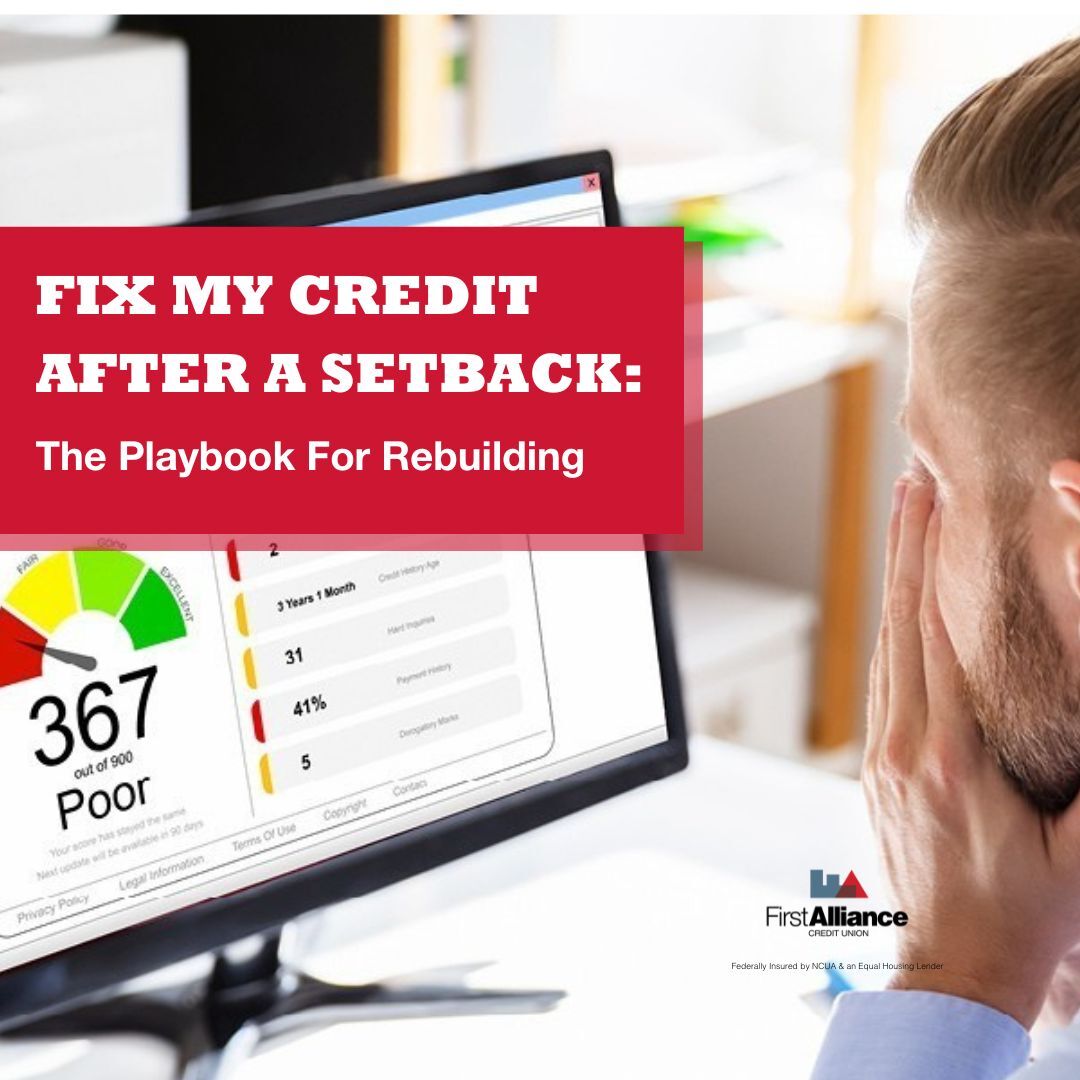

Jaden should have floated out of graduation. ESPN had just handed him a remote‑work contract; his retail apron was history. But one number yanked him back to earth: 580. Three grand in burritos, sneakers, and late fees had maxed his only card, and missed payments dotted his credit history like pepperoni on a pizza. Determined to turn the page, he walked into First Alliance Credit Union, exhaled, and said, “Fix my credit…please.”

Here’s the six‑step comeback plan we mapped out for him—no shame, no fluff—so you can borrow it for your own credit rebound.

Before changing anything, Jaden needed the full picture. The U.S. has three credit bureaus—Equifax, Experian, and TransUnion—and each keeps its own file. One mistake in just a single bureau can drag down your score everywhere, so he downloaded all three reports free from AnnualCreditReport.com. He highlighted an unfamiliar medical collection, uploaded proof it wasn’t his, and filed an online dispute. A week later, the bogus debt disappeared and his score climbed 18 points before the first ESPN paycheck even cleared.

Quick‑wins

Pull all three reports—free, weekly.

Circle any item that’s wrong (balance, dates, accounts you never opened).

File disputes online; bureaus must investigate within 30 days, and checking your own report never hurts your score.

Payment history drives 35 percent of a FICO® score, so every on‑time check‑in counts. Jaden set automatic minimum payments for payday, eliminating “oops” fees for good. He then called his issuer, politely explained his new salary, and secured a one‑time late‑fee reversal. Finally, he tackled overdue bills in order of damage:

Accounts 60+ days late (hurt the most)

Balances nearest their limits

Everything else by due date

Within three months, a bright‑red “delinquent” tag turned gray—another 25‑point boost.

Credit utilization shows how much of your revolving credit you’re using: balance ÷ limit. A $300 balance on a $1,000 limit equals 30 percent utilization; lenders prefer anything below that number.

Jaden started snowballing cash—every spare dollar from textbook sales, side‑gig money, and the $20 saved by skipping DoorDash—onto one balance until it vanished. Freed‑up dollars snowballed to the next card, and momentum grew. After three spotless months he asked for a modest limit increase; the issuer bumped his limit to $4,000, slicing utilization 25 percent overnight without new spending. He now sticks to charging no more than 10–30 percent of his limit and paying in full each month.

Quick‑wins

Pay more than the minimum payments each week until utilization drops under 50 percent.

Request a limit increase after three on‑time payments.

Keep future balances below 30 percent—and ideally under 10 percent—for the best score gains.

Credit scores don’t sprint; they jog—steady, predictable, and faster than you might think when you stick to the plan. Here’s the mile‑marker map so you know what to expect:

| When | What’s changing under the hood | Typical score bump* |

|---|---|---|

| First 30 days | Disputed errors fall off, new credit‑limit bumps post, and your balance‑to‑limit ratio drops. | +15–40 pts |

| Months 3–6 | Six perfect payments form a clean streak, nudging old late marks into the background. | +40–60 pts |

| Month 12 | A full year of low balances, mix of loan + card, and zero fresh dings proves you’re steady. Scores in the high‑600s are common. |

*Every file is different, but momentum is real.

Why these jumps matter to you

First month wins: Fixing mistakes and lowering utilization are the quickest points you’ll ever earn—often before your next billing cycle closes.

Quarter‑year lift: Payment history is the biggest slice of your score pie. Nail six on‑time payments, and the algorithm starts “forgiving” yesterday’s stumbles.

One‑year milestone: Time becomes your teammate. A 12‑month streak turns you from “risky” to “reliable,” unlocking better rates, easier approvals, and smaller security deposits.

Heads‑up: If someone promises overnight miracles—like wiping legit late payments in a weekend—walk away. Real credit repair follows this clock: consistent actions, compounding month after month, until your new score pops up in bold on the next credit pull. Stick with it, and the celebration text you’ll send yourself in a year will feel so good.

A repaired score needs protection or it will slide back. Jaden adopted a zero‑based budget—every dollar earned already has a job (rent, groceries, debt, savings) so the month ends at zero unassigned cash. Spontaneous spending no longer creeps onto plastic, and surprises get covered by his growing emergency fund, not a credit card swipe. Weekly reviews keep categories honest, and free score alerts in the First Alliance app help him dispute any suspicious activity within days.

| Play | Result |

|---|---|

| Deleted bogus collection | +18 pts |

| Utilization cut to 25 % | +32 pts |

| Six‑month on‑time streak | +45 pts |

| Credit‑builder loan half paid | +15 pts |

| New FICO® Score | 690 |

Today, loan offers arrive with single‑digit rates, apartment applications sail through without a cosigner, and yes—he still buys kicks, but now he swipes a cash‑back card and pays it off the same day. The comeback feels good.

Credit setbacks aren’t character flaws—they’re fixable stats. Drop by a First Alliance branch or tap Join online. We’ll listen to your story, map out clear next steps, and help you celebrate every point‑by‑point victory. When that triumphant score update pings, you too can say, “Look how far I’ve come.”

1 min read

Credit cards are a big responsibility. If you are thinking about getting a credit card, make sure it's the right one for you. While credit cards can...

1 min read

Picture this: you’re grabbing snacks after school, and the cashier asks, “Credit or debit?” Both cards look alike, but they pull money from very...

1 min read

Back in the late ’70s, when Abuela Carmela first arrived in Texas without the residency papers banks demanded, she tucked every hard‑earned dollar...