Chris Gottschalk

Chris Gottschalk

1 min read

How to Get Money Fast

One of the worst parts of any financial emergency is having to come up with the cash to get through it. This can be stressful even if you have a...

Financial emergencies can happen at any time to anyone. You might get into your car only to discover the engine is dead, discover that your house needs to be reshingled after a severe thunderstorm or break a bone during a ski trip.

No matter what the emergency is, it’s expensive, and it’s going to cost hundreds, if not thousands, of dollars to set right. If you have a robust emergency savings account, the odds are good that you’ll be able to cover the expenses, although you might feel some financial strain. If money is already tight, though, you’ll probably be worrying about how you’ll be able to pay for the emergency without having to declare bankruptcy.

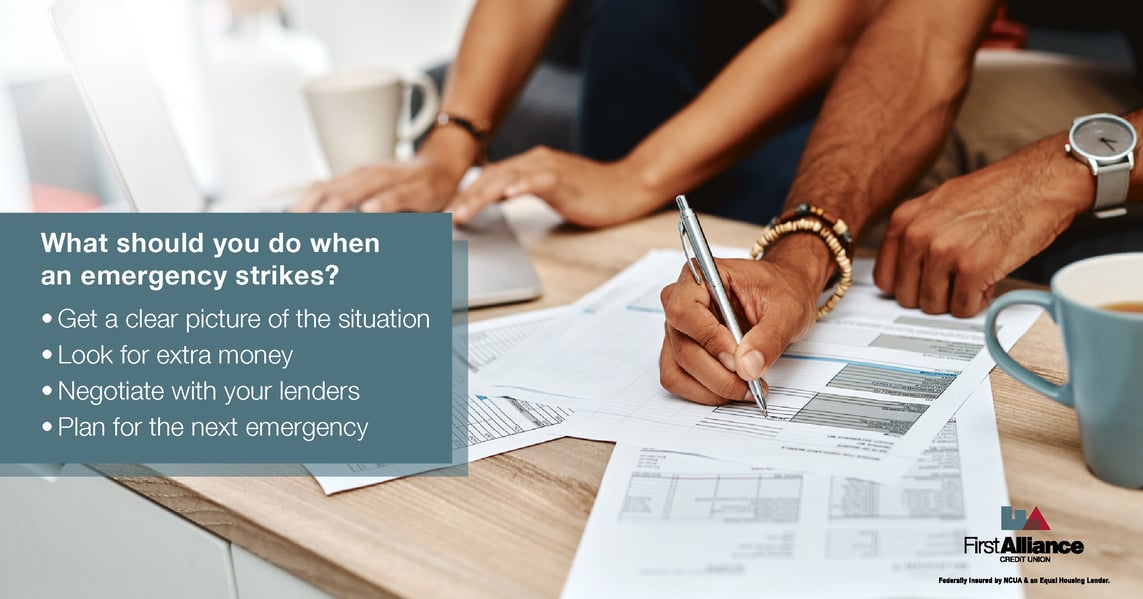

If you do get hit with a financial emergency, remember—you’re not helpless. You can take some steps to pay off the bills the emergency incurred, lessen the financial impact on you and your family and get back on your feet.

After you’ve been struck by a financial emergency, don’t panic. It won’t help your situation, and you’ll only stress yourself out further. Instead, take some time to evaluate your situation. Ask yourself what you’ll need to do to take care the financial emergency, and try to get a sense of how much it’s going to cost.

When thinking about the costs, be honest with yourself. The final amount will be a psychological blow, but this is the time to face the reality of your situation head on. The sooner you have an idea of how much you’ll have to spend, the more prepared you’ll be to handle the challenge of paying for everything.

Once you know how much money you’ll need, start looking for extra money to throw at the problem. Ideally, you have an emergency fund with enough money in it to take care of the emergency. If you do, now is the time to use it to pay off your bills as much as possible.

However, if you don’t have that much money saved, you still have some options. Your first order of business should be to go through your budget and start cutting expenses.

When going through your budget, make sure you set aside the money you need to survive first. This should include money for food, shelter and utilities, as well as any monthly expenses associated with doing your job. You should also look at any other loans you’re still paying down.

After that, look at your nonessential expenses, such as clothing, entertainment and eating out, and then start cutting wherever you can. This will not be fun, but the goal for now is to set more money aside from your paycheck to expedite your financial recovery.

It’s worth pointing out that even small cuts can add up to a lot of money. For instance, if you unsubscribe from three streaming services and stop buying a cup of coffee each morning, you’ll have about $100 a month to throw at your bills. That’s $1200 a year!

Once you’ve cut nonessential expenses, your next step is to talk with financial institutions. You might be able to take out a personal loan or a personal line of credit to help you cope with the expenses.

If you’re really hard up for money, you can also swallow your pride and ask friends and family members if they can loan you some cash. However, this can put a strain on relationships, so be careful if you decide to go this route.

You might be tempted to withdraw money from your retirement fund to help pay for the emergency, but this is a bad idea. Withdrawing this money can put your retirement at risk, and you may also have to pay taxes and penalties for early withdrawal. You’ll also want to avoid using credit cards, unless they have a low interest rate.

Your next step should be to contact your lenders immediately and start negotiating with them. Believe it or not, most lenders are willing to work with you during a financial emergency, especially since it might mean the difference between getting less money than they were planning on and getting none at all.

Lenders might be able to temporarily lower your interest rates, extend the terms of your repayment plan or even grant you a forbearance so you don’t have to make any payments at all if your emergency is short term. Just be sure to contact them as soon as you know you’re in trouble. If you wait until you start receiving delinquent notices, you’ll have a lot less options.

Step Four: Plan for the Next Financial Emergency

Step Four: Plan for the Next Financial EmergencyOnce you’ve gotten through your current hardship, take a few moments to catch your breath and congratulate yourself. After that, though, you'll want to make preparing for future financial emergencies a high-priority financial goal.

The best place to start is by building up your savings. Most financial experts agree that you should have at least three months of salary in your emergency fund, although the ideal amount would be six months. Once you have at least three months of salary saved up, though, you can start to rest easier.

If you've had to reduce unnecessary expenses in order to deal with the emergency, you might want to keep those expenses reduced. Chanel that money toward your emergency fund instead. If you get any extra income, you should put that toward your emergency account as well.

While you're rebuilding your emergency fund, you should also consider what type of bank account is the best one for it. A traditional savings account is a great choice if you're taking your first steps toward rebuilding your emergency fund, however, there are other options once you have more money saved. A money market account, for instance, will give you a higher interest rate, yet still keep your money accessible by debit card.

You may also want to look at your insurance plans and see just what they cover. Many people don’t know what the insurance plans for their health, cars and homes actually cover, and as a result most people get taken by surprise when they have to use those plans. You might also want to take some time to shop around to try to improve your coverage, reduce your rates or both.

The time it takes to recover depends on several factors, such as the severity of the emergency, how much money is in your emergency fund and whether you have to borrow additional money. It's worth pointing out that the more you have in your emergency fund, the faster you'll recover.

Unexpected financial emergencies can happen at any time, from car repairs to job loss. When they do, you’ll want to evaluate the situation, prioritize your expenses and try to get some assistance if you need some financial aid.

You can also use the resources First Alliance Credit Union offers to help you get through any financial emergencies that arise. We offer services to members that are going through financial hardship, such as our Anytime Skip a Pay form, and our lending advisors can help you refinance your loans to get a lower monthly payment and consolidate your debts. First Alliance also offers financial guides, such as our beginner’s guide to budgeting that will help you allocate your money most effectively, and calculators that will help you do anything from figure out a budget to the length of time you’ll need to pay off your credit cards.

1 min read

One of the worst parts of any financial emergency is having to come up with the cash to get through it. This can be stressful even if you have a...

1 min read

Life has a funny way of throwing curveballs when you least expect them.

1 min read

Seventeen-year-old Noah always dreamed of bigger things: a car with more legroom, his own place with a balcony view, and the freedom to grab tacos...