1 min read

Give Yourself a Financial Wellness Boost! How to Start Saving Money

Saving money is tough. In fact, as humans, we're wired to take care of our needs now, and worry about later...well, later. Putting resources away for...

6 min read

Life has a funny way of throwing curveballs when you least expect them.

One day everything feels steady. Next, your car won’t start. The furnace quits, and a medical bill shows up when you least expect it.

Those moments are stressful enough on their own. The last thing you need is financial panic piled on top of everything else.

That’s where an emergency fund comes in. It’s one of the simplest and most powerful ways to protect your peace of mind. And here’s the part a lot of people need to hear: you do not have to be wealthy to start one. You just have to start.

An emergency fund is money you set aside specifically for unexpected expenses and leave untouched until you truly need it.

Think of it as your financial safety net.

It’s the money that keeps your life steady when something unexpected tries to knock it off balance.

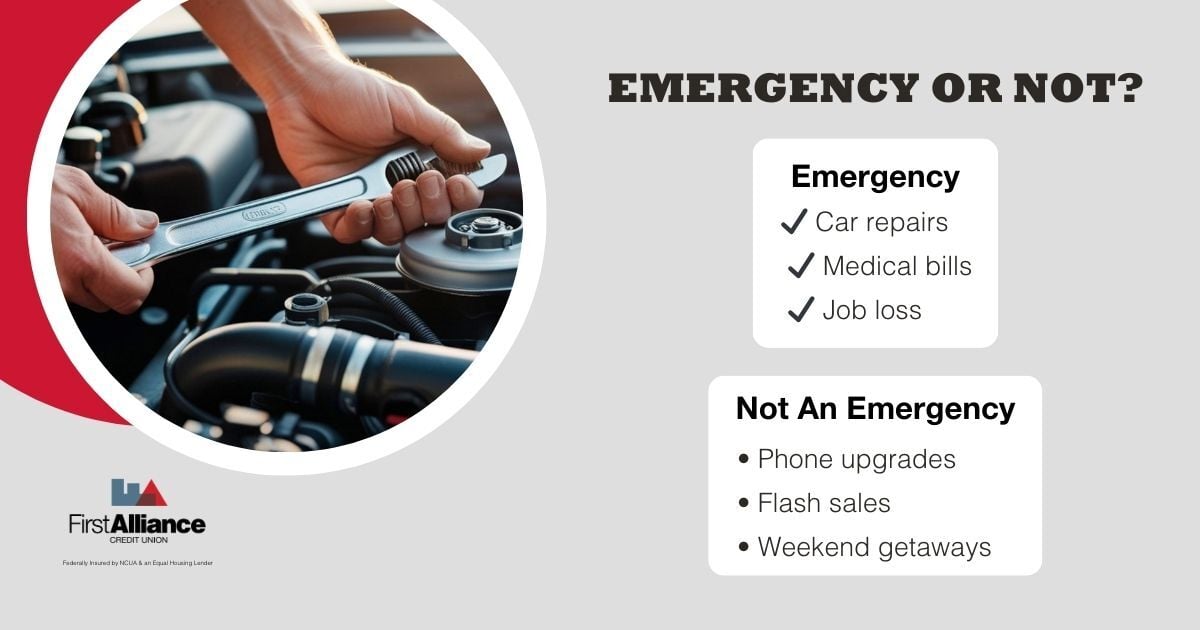

|

Emergencies include: |

Not emergencies: |

|

Car repairs |

The latest phone upgrade |

|

Medical bills |

Flash sales |

|

Major home repairs |

A spontaneous weekend trip |

|

Job loss or reduced income |

Eating out more than planned |

And listen, it’s completely human to blur that line sometimes. We all do it. That’s why keeping your emergency savings separate and intentional really matters. It protects you from those in-the-moment decisions that feel urgent but really aren’t.

You’ve probably heard the recommendation: 3 to 6 months of living expenses.

That might sound like a lot, and honestly, it kind of is. But the reasoning is solid. If you were to lose your job tomorrow, it can take time to find a new one, and your bills aren’t going to pause while you search. Having a cushion that covers your essentials for a few months gives you breathing room to make smart decisions instead of desperate ones.

Here's the thing though: three months of expenses can feel impossibly out of reach when you're just getting started. And that is completely okay. You don't need to get there overnight. The important thing is to begin, even if it's small. Saving $5 or $10 at a time still counts. Every single dollar you put away is one more dollar working in your favor. There's no amount too small to matter.

Before you can decide how much to save, you need a clear and honest picture of your spending. Pull up your bank statements from the last one to three months and really look at where your money is going. Highlight the purchases that weren't exactly necessary. The extra coffee runs, the impulse online orders, the subscription you forgot you were still paying for. You might be surprised at how much is quietly slipping through the cracks.

This isn't about shaming yourself over past spending. Not at all. It's about getting real with yourself so you can make room for saving. Even freeing up $50 a month can make a meaningful difference when you're consistent about it over time. Progress is progress, no matter how small it looks at first.

Here's one of the best habits you can build around saving: the moment your paycheck hits, move a set amount directly into your emergency fund before you spend anything else. This is what's known as "paying yourself first," and it is surprisingly effective.

Why does it work? Because if the money is still sitting in your checking account, it's easy to tell yourself you'll transfer it later. And then later never comes. But when you move it right away, you naturally adjust your spending to whatever's left. Out of sight, out of mind.

The easiest way to make this consistent is through automation. Set up an automatic transfer from your checking account to your savings account on payday. That way, you never have to think about it, debate it, or talk yourself out of it. It just happens, and your savings quietly grows in the background. Many people say this one simple change was the thing that finally made saving feel doable. You might find the same.

Your emergency fund needs to live somewhere safe, accessible, and separate enough from your everyday checking account that you’re not tempted to casually dip into it. A few solid options:

A regular savings account is the most straightforward choice. It’s easy to open, easy to access when you need it, and keeps your emergency fund clearly separate from the money you spend day to day.

If you're getting started, First Alliance's WINcentive Savings Account is a fantastic option. Designed with first-time savers in mind, it offers all the basics of a regular savings account – easy access, a safe place to grow your fund – plus the chance to win cash prizes just for saving. It's a great way to build the habit while staying motivated.

A money market account is worth graduating to once your fund reaches a certain level, typically around $2,000 or more. These accounts tend to earn a higher interest rate, so your money works a little harder while it waits.

Think of moving into a money market as a savings milestone to aim for. Start with a regular savings account, build the habit, and once you hit that $2,000 mark, upgrade and start earning more on everything you've saved. It's a great goal to work toward.

One thing to avoid: certificates of deposit, or CDs. While they often come with attractive interest rates, they lock your money up for a set period of time. If an emergency hits and your funds are tied up in a CD, you could face penalties for withdrawing early, which defeats the whole purpose of having the fund in the first place.

This is a real challenge a lot of people face, and if this is you, you are not alone. You want to build your emergency fund, but you've also got credit card balances or loan payments eating into your paycheck every month. So what do you do?

The answer doesn't have to be all-or-nothing. One approach that works really well is consolidating your debts, rolling multiple high-interest payments into one lower monthly payment. That frees up money you can then split between paying down debt and building your savings at the same time. Take the amount you're saving from consolidation and put half toward extra debt payments, and put the other half into your emergency fund. It's slower than going all-in on one or the other, but you're making progress on both fronts simultaneously. That matters.

If you're not sure how to navigate this, sit down with someone at your financial institution. A good banker can look at your full picture and help you build a plan that actually fits your life, not just hand you a generic checklist.

One of the biggest traps people fall into is setting their savings contribution too high right out of the gate. It sounds counterintuitive because isn't saving more always better? But if you're moving more money into savings than your budget can realistically handle, you'll end up pulling it back out for non-emergency expenses. And once you do it once, it gets easier to justify doing it again. Before long, the fund never really grows.

Start with an amount that genuinely won't strain your everyday life. Even $25 or $50 per paycheck is a real, legitimate starting point. You can always increase it later once the habit feels natural. Be kind to yourself through this process.

Here's something really important: if you drain your emergency fund because an actual emergency happened, that is not a failure. That is the fund doing exactly what it was built to do. Please give yourself some grace.

Once the dust settles, go back to your budget. Can you temporarily bump up your contributions to rebuild faster? Did something in your financial situation change that gives you a little more wiggle room? Or do you need to scale back for a while and just save what you can? All of those are valid answers. Building an emergency fund isn't a straight line. It climbs, sometimes it drops, and then it climbs again. That's not you doing it wrong. That's just life.

It's easy to put off saving for emergencies when things feel stable. But the time to build your safety net is before you need it, not in the middle of a crisis. Even the smallest steps add up, and there's a genuine sense of calm that comes from knowing you have something to fall back on.

Start small. Automate what you can. Be patient with yourself. And do not hesitate to ask for help, whether that means sitting down with someone at First Alliance Credit Union to review your budget, explore debt consolidation options, or choose the right savings account for your goals. Having a local team that knows you and genuinely wants to see you succeed can make all the difference.

Life will always have its surprises. The best thing you can do is make sure you have the right support behind you and a plan that helps you feel ready for whatever comes next. At First Alliance Credit Union, we’re here to help you take the first step, and every step after. Whether you’re looking to open a WINcentive Savings account, talk through your budget, or explore options for managing debt, our team is ready to work with you. Your financial peace of mind is worth it, and we’d love to help you get there.

1 min read

Saving money is tough. In fact, as humans, we're wired to take care of our needs now, and worry about later...well, later. Putting resources away for...

1 min read

It is never too soon to start saving for events that occur later on in life such as retirement. In fact, if you wait too long, it is simply not...

.jpg)

1 min read

Setting savings goals is a crucial step towards financial stability and independence. It provides a clear path to follow and helps you stay focused...